The British tech sector can rest a little easier tonight after the UK arm of Silicon Valley Bank (SVB) was sold to HSBC for just £1.

The intervention followed last week’s collapse of the subsidiary’s California-based parent company. The Bank of England (BoE) intervened over fears that mass withdrawals in the US would spread to the UK business.

Many of SVB UK’s 3,300 customers, which include numerous VC investors and startups, warned they would go bust if their deposits were lost. The BoE had initially planned to put the bank into insolvency, which would have only guaranteed protection for deposits worth up to £85,000, or £170,000 for joint accounts.

The deal with HSBC supersedes the insolvency plan. Customer deposits can now be protected without requiring taxpayer support.

“This action has been taken to stabilise SVB UK, ensuring the continuity of banking services, minimising disruption to the UK technology sector, and supporting confidence in the financial system,” the BoE said in a statement.

After the deal was announced, SVB UK said it was resuming normal operations.

Following the announcement that @HSBC_UK has acquired SVB UK, we’re resuming normal operations from today. Our clients should not notice any significant changes, however, there may be short delays across the next few days as we return to business as usual. Thanks for the support

TechUK, an industry lobby group, said the sale will be a relief for the British tech ecosystem.

“Without access to their deposits these companies faced the prospect of not being able to pay staff or rent or suppliers — in short many would also be facing insolvency and the many thousands of people working in this part of the tech sector would be very worried about their jobs!” said techUK CEO Julian David.

For HSCB, the acquisition of all SVB UK’s assets for a nominal £1 could be an extremely good deal. The Bank of London, which had also submitted a rescue bid, described the sale as a “missed opportunity.”

“It cannot be right that once again the heritage banks that have provided a poor service to UK entrepreneurs over many years benefit from their already dominant position,” the clearing bank said in a statement.

Legal experts are already pointing to the lessons for startups. Charles Fletcher, a partner at law firm Mishcon de Reya, recommended several steps that businesses can take to avoid the risks that SVB UK has exposed.

“Key actions include keeping corporate accounts with more than one bank, having an emergency funding plan to avoid cashflow squeezes, separating funds from different sources and taking a strategic approach to managing currencies,” said Fletcher.

“These should accompany fundamental business planning and management steps, such as a detailed risk register and crisis management protocols.”

The EU Commission is extending the relaxation of state aid rules to prevent green tech firms from relocating abroad and enable the bloc’s transition to a net-zero economy.

The rules around national subsidies had already been amended in 2022 as a response to Russia’s war on Ukraine, seeking to enable member states to more easily finance struggling companies and energy production in Europe.

Now, rising concerns about an escalating global subsidy race have pushed the EU to further prolong this temporary crisis framework — and even expand its scope to include support to domestic clean tech companies fighting climate change.

The move seems to be heavily influenced by the US’ Inflation Reduction Act (IRA), which offers $369 billion in subsidies for green technologies “made in America.” This has triggered fears that EU companies will be tempted to relocate their business to the US.

To avoid a potentially catastrophic blow to the bloc’s long-term competitiveness in the green tech industry, the Commission has adapted the state aid rules to streamline the approval of subsidies for companies that accelerate the rollout of renewable energy, energy storage, and the decarbonisation of industrial production processes.

The EU has targeted six main sectors: batteries, solar panels, wind turbines, heat-pumps, electrolysers, and carbon capture usage and storage. This also includes production of key components as well as the manufacturing and recycling of related critical raw materials.

“The framework gives member states the option to offer aid in a fast, clear, and predictable way.

The amended rules will provide member states with more flexibility to inject public funds, allowing for higher aid ceilings and simplified aid calculations.

SMEs and companies located in disadvantaged regions are eligible for higher support, while EU nations can also access larger funds if the aid is provided via tax advantages, loans, or guarantees.

To prevent cases in which the risk of relocation is high, countries will have a “matching aid” option. That is, to match the subsidies offered by a non-EU government and keep the company within the union’sborders. Alternatively, member states will be able to cover the funding gap the company expects to have.

“Our rules protect the level playing field in the single market.

To ensure that these options don’t provoke unfair competition in the bloc, the Commission has put three safeguards in place:

The aid can be granted to companies in less developed areas, or to projects located in at least three member states.

Eligible companies need to use state-of-the-art production technology from an environmental emissions perspective.

The aid cannot trigger relocation of investments between member states.

EU countries can make use of the new rules until 31 December, 2025, but disbursements could continue afterwards as well.

“The framework that we have adopted today gives member states the option to give state aid in a fast, clear, and predictable way,” Margrethe Vestager, Executive VP in charge of competition policy, said in a statement.

“Our rules enable member states to accelerate net-zero investments at this critical moment, while protecting the level playing field in the single market and cohesion objectives. The new rules are proportionate, targeted, and temporary.”

Ioanna is a writer at SHIFT. She likes the transition from old to modern, and she’s all about shifting perspectives. Ioanna is a writer at SHIFT. She likes the transition from old to modern, and she’s all about shifting perspectives.

Under the Chips Act, the EU is seeking to end its dependence on China and produce 20% of the world’s semiconductors by 2030. Amidst the political push, attracting global giants to invest in the union’s domestic production has been a key strategy — with Intel’s plan to construct a massive chip plant in Magdeburg, Germany, considered a big boost for the bloc.

But now, Intel is asking the German government for an additional €4 billion to 5 billion in subsidies to move forward with the project, Bloomberg reports, citing people familiar with the matter.

In March 2022, Intel announced an initial investment plan of over €33 billion (reaching €80 billion within the next decade) to strengthen the EU’s semiconductor industry across the entire value chain. This included the megasite in Germany, a new chip research centre in France, a back-end manufacturing facility in Italy, and the expansion of its existing chip factory in Ireland, lab in Poland, and supercomputing centre in Spain.

Construction of the much-anticipated semiconductor factory in Magdeburg was postponed at the end of last year due to economic hurdles, as a result of the high energy prices and inflation following Russia’s war on Ukraine, according to the report.

Artist’s impression of Intel’s chip plant in Germany. The factory is expected to generate 3,000 high-tech jobs. Credit: Intel

Intel had initially estimated that the project would cost €17 billion and had reached an agreement for €6.8 billion in government subsidies. Now, however, the company expects to spend €30 billion — thus requiring further government aid. It’s also open to tax breaks or energy subsidies.

“Disruptions in the global economy have resulted in increased costs, from construction materials to energy,” Intel said in a statement. “We appreciate the constructive dialogue with the federal government to address the cost gap that exists with building in other locations and make this project globally competitive.”

According to Bloomberg, Intel is likely to delay its project in Italy as well, and is currently in discussions with the Italian government. On the plus side, the research centre in France and the facility’s expansion in Ireland seem to be on track.

EU Commission President Ursula von der Leyen has characterized Intel’s investment as “the first major achievement” under the new Chips Act. “It’s a considerable contribution to the European chips ecosystem that we’re building right now,” she commented after the tech giant’s announcement.

The continent’s weak position in the global semiconductor market was especially evident during the pandemic, demonstrating that chips are integral to the EU’s digital and green transitions as well as its geopolitical agenda. But although the bloc has managed to attract a numberof investors, it seems that fully enabling their project still remains a challenge.

Get the TNW newsletter

Get the most important tech news in your inbox each week.

No one may fully understand quantum computing yet, but one thing is clear — the expectations are high. And where there are high expectations, there’s money.

Both private and public funding for European quantum technologies has grown notably over the last few years. In 2021, private funding to quantum startups increased by 2.5x compared to 2020, and by 8x compared to 2019. Public funding has grown as well, with the EU planning to invest $7.2 billion (€6.8 billion) in quantum computing projects by 2025.

Understandably, most of these billions already are or will be directed to building a successful quantum computer — hardware is currently the biggest bottleneck in the deployment of this technology. However, let’s not forget that hardware alone won’t be enough. Without suitable software, quantum computers will have no value.

Yet, quantum software gets undeservedly little attention and, thereby, funding.

A quantum “chicken or the egg” challenge

An obvious example that quantum software in Europe is being undervalued is the money distribution in the EU’s Quantum Technology Flagship program — the ambitious initiative to support Europe’s quantum innovations with a total of €1 billion in funding. The first phase of this initiative has concluded with €152 million invested. Of those, just €4.6 million — that’s a mere 2.9% — were directed to the research and development of quantum software.

When it comes to private investments, the situation is better, albeit similar. In 2021/2022, about 14.5% of equity investments into European quantum computing startups were directed to software solutions. And it seems that in 2023, this trend continues. Europe’s quantum computing startups that have raised noteworthy rounds this year — including Pasqal (€100 million), Quantum Motion (£42 million), Oxford lonics (£30 million) — are all hardware-focused.

In the tech world, such focus on the hardware is unusual — in any other field, software typically receives the largest share of investments due to easier scalability and greater profit opportunities. So why, when it comes to quantum tech, it’s the other way around?

The reason for this anomaly is this: both private investors and public funds see quantum computing as a hardware problem rather than a software problem. And to some extent, they’re right — building successful quantum hardware is indeed the most burning challenge. Well, right now. But in the big picture, it’s only one-third of the problem.

The three hurdles to jump

When it comes to quantum computing, there are three central problems we still need to solve.

The first and most obvious one is to build a quantum computer. There are currently no quantum computers used for more than experiments, so this is what the industry is mainly focused on — from the world’s tech giants, such as Google and IBM, to startups and academia.

The second challenge is to reduce errors in quantum computers, enabling them to perform longer computations. Better hardware will reduce errors, but is unlikely to be sufficient by itself. We must find ways to correct quantum computing errors at the software level.

And the third problem is to find more computing methods for quantum computers, that is, quantum software applications. Quantum computers will be useful for modeling physics and chemistry, but the extent of their usefulness for data processing — from machine learning to planning and scheduling — is less clear. If we could find a couple more methods to expand the scope of problems these computers can solve, that would bring fundamental progress.

Hence, two of the three central quantum computing problems are software-related. But how come this isn’t at all reflected in the distribution of funding? Given that we’re pouring all (okay, most) of the available money into hardware, how is anyone expecting to be able to use this new supercomputer without the “brain” that actually powers it?

It might not be a software problem today, but it will be tomorrow

A reasonable distribution of funding, to my opinion, would be 15-20% for quantum software and 80-85% for hardware.

Quite simply, hardware is the most expensive and complex part of this technology, so it’s rational to allocate the largest amount of funding to it to expedite development. And directing one fifth of the total funding to software would be sufficient to cover the R&D work on new quantum computing applications.

While the distribution of private investments doesn’t look that hopeless, the EU’s public funds are lightyears away from reaching this goal.

Look, the development of quantum software takes years. It took my colleagues and me between five and 10 years to develop quantum walks as a method for solving problems. I expect a similar timescale for new problem-solving methods of comparable or larger significance.

What concerns me is that if we continue neglecting quantum software, in just about 10 years, quantum computing will become a software problem — and a life-or-death one. There will be quantum computers with applications mainly in physics and chemistry. In other areas, they will still be mostly used for experimentation rather than for actual problem-solving.

In other words, Europe’s now spending billions on specialised computing devices that it might not know how to adapt to wider applications. And if we aren’t able to provide software that would expand the application of these devices, we risk losing interest in this technology and its further development altogether. The range of applications will simply be too small for the world to care.

Ioanna is a writer at SHIFT. She likes the transition from old to modern, and she’s all about shifting perspectives. Ioanna is a writer at SHIFT. She likes the transition from old to modern, and she’s all about shifting perspectives.

The European Commission has launched a new €7.5 million grant scheme to help Ukrainian SMEs integrate and benefit from the single market.

The so-called ReadyForEU scheme comprises two calls for proposals directed to Ukraine-based businesses and entrepreneurs: the Business Bridge and the Erasmus for Young Entrepreneurs — Ukraine. The calls follow the country’s recent entrance into the singlemarket programme, which is also providing the funding.

“ We’re offering tangible financial support for small Ukrainian businesses and entrepreneurs.

The Business Bridge

With a budget of €4.5 million, this action offers financial support to SMEs affected by the war, in the form of vouchers. These will enable the companies to access services and take part in trade fairs in the EU.

A dedicated consortium of business organisations will select up to 1,500 growth- and sustainability-oriented Ukrainian SMEs, which will receive up to €2,500. The grant’s purpose is to cover costs related to business support services, such as legal, financial, or organisational advice.

According to the Commission, the call will not only support companies involved as well as boost the reconstruction of the Ukrainian economy, but also provide alternative markets to EU businesses, following the loss of the Russian and Belarusian markets.

The Erasmus for Young Entrepreneurs — Ukraine

With a budget of €3 million, the second call aims to enable new Ukrainian entrepreneurs to gain business experience in other European countries.

It will select organisations in the Ukraine and the EU to recruit up to 430 entrepreneurs and match them with host entrepreneurs based in the bloc. It will also provide them with financial support and contribute to their living and travel expenses.

“Europe is committed to supporting Ukraine’s successful integration in the single market,” Thierry Breton, Commissioner for Internal Market, said in a statement. “With today’s calls for proposals, we are offering tangible financial support for small Ukrainian businesses and entrepreneurs to build new partnerships with other European companies and expand into the EU.”

Ukrainian SMEs and entrepreneurs will be able to apply in the final quarter of this year.

Get the TNW newsletter

Get the most important tech news in your inbox each week.

Rishi Sunak has enraged British scientists after dimming hopes of rejoining the EU’s Horizon programme.

Prospects of reentering the €96 billion research scheme had grown after a new Brexit deal for Northern Ireland was struck on Monday. European Commission president Ursula von der Leyen described the agreement as “good news” for scientists and researchers. She said work to associate the UK with Horizon could start “immediately” after implementing the terms.

Scientists had overwhelmingly welcomed the breakthrough. Sir Adrian Smith, President of the Royal Society, the UK’s foremost collective of scientific voices, called for access to Horizon to be swiftly secured.

“These schemes support outstanding international collaboration, and the sooner we join them, the better for everyone,” Smith said in a statement. “The government has stated that the UK is more committed than ever to strong research collaboration with our European partners.”

This optimism quickly faded. According to a new report in Financial Times, Prime Minister Sunak is “sceptical” about the benefits and cost of Horizon. Officials said Sunak will review other options, including a new global research collaboration.

The news sparked fury among scientists.

“This is unspeakably idiotic.

As the world’s biggest research programme, Horizon has been praised for enhancing collaboration, research standards, and supply chains for businesses — all of which are now at risk for the UK. Scientists fear that a continued absence from the scheme will lead British R&D to fall behind globally.

Dr Mike Galsworthy, a researcher and campaigner described Sunak’s plan as “unspeakably idiotic.”

“To be a science superpower or anything close to it, we need to rejoin Horizon enthusiastically… and *theninvest in conferences, meetings, and new mechanisms to rapidly re-establish the UK as a European team leader,” Galsworth said in a tweet. “So WHAT is Rishi Sunak playing at?”

Opposition politicians have also slammed the intervention. Chi Onwurah, a shadow science minister and former engineer, noted that the ruling Conservative party previously promised to associate with Horizon.

“No Plan B can match Horizon Europe for funding, influence or range,” she said. “Breaking this promise would be a massive Sunak failure.”

Britains science and business know association w Horizon Europe is in the country’s best interests. Tory 2019 manifesto promised to achieve it. No Plan B can match Horizon Europe for funding, influence or range. Breaking this promise would be a massive Sunak failure. https://t.co/guc7TTfkNL

Debate is raging about Sunak’s motivations. Some observers suspect he wants to do genome research that the EU would find unethical, while others argue that his stalling is merely a negotiating ploy.

Regardless of his tactics, researchers want a quick return to Horizon — before the UK’s international standing is further damaged

Why can’t European tech companies compete with Silicon Valley giants? It’s a perennial conundrum for the continent’s IT leaders — and one that Phill Robinson is trying to solve.

After a globetrotting career as a tech executive, Robinson returned home to the UK and founded Boardwave, a networking platform that wants to make Europe a software superpower.

The concept emerged from Robinson’s diverse background in the sector. The entrepreneur spent decades traversing Europe and Silicon Valley, in roles ranging from CMO of Salesforce.com during its IPO to CEO of Dutch software giant Exact.

These experiences exposed several advantages for tech firms in the US. Robinson zeroed in on one: the breeding ground for success created by Silicon Valley’s tight-knit community. The small area of land interconnects a multitude of tech whizzes, entrepreneurs, investors, and advisers. In Europe, meanwhile, the business environment is highly fragmented.

To emulate the valley’s network effects, Robinson founded Boardwave. At TNW Valencia on 30 March, he promises to share further insights on building tech giants.

Ahead of the talk, Robinson unveiled one of his most ambitious proposals: creating a pan-European version of Nasdaq.

Robinson wants Boardwave’s online platform and in-person events to create new connections for European software firms. Credit: Boardwave

Nasdaq is the world’s premier marketplace for tech stocks. Google, Amazon, Apple, Facebook, and Microsoft all went public on the exchange. In Europe, there’s no comparable trading venue, which restricts the growth of startups.

“There isn’t a single tech market here in Europe,” Robinson tells TNW. “Nor is there the knowledge, experience, and understanding of software from investors in public markets. They don’t know how to value software companies, they don’t understand how they operate, and they don’t understand the intrinsic value of them.”

These circumstances contribute to a vast “exit gap” between European and US firms. In Europe, tech founders often sell their businesses while they’re still private — and miss the chance to maximise their valuations on the public market.

Those that do pursue an IPO typically list in the US.

“Either they go on the NYSE or on the NASDAQ,” says Robinson. “At that point, you’re not a European software company anymore — you suddenly become a US software company.”

Arm’s hammer blow

Arm’s flotation plans provide a painful example of the impacts. The British chip giant is set to snub pleas from the UK government to list in London and instead float in New York. Even offers to bend stork market rules have failed to convince the company to go public in its home country.

Analysts attribute the decision to the US investment landscape’s bigger equity markets, focus on growth, and history of generating higher valuations. European investors, by contrast, have a reputation for being risk-averse and short-termist.

A Nasdaq listing also increases confidence that a company will be around for the long haul.

“It’s a step towards being a global leader, which we don’t have in Europe,” says Robinson.

It’s a market for technology businesses to go public in Europe.

Proposals have been floated for a localised equivalent of Nasdaq in Paris or London. But Robinson insists that only a pan-European exchange would have the necessary scale.

Founding such a market will be immensely challenging. It requires the will of politicians, new legislation, and deeper market expertise. Once those are in place, European tech firms will need to be persuaded to list on the market.

It won’t be an easy process, but Robinson is convinced it would be worth the effort.

“If you have a European version of Nasdaq… it’s a market for technology businesses to go public and list their companies in Europe — and not sell out to become an American software company by virtue of the fact there’s nowhere else to go.”

Phill Robinson will be speaking at TNW València, which takes place at the end of March. If you want to experience the event, we’ve got something special for our loyal readers. Use the promo code TNWVAL30 and get a 30% discount on your conference business pass for TNW València.

A new €15 million fund has launched to help quantum technology research in the Netherlands transform into venture capital-investable startups.

Backed by Quantum Delta NL (QDNL), a foundation that seeks to boost and scale the Dutch quantum ecosystem, the so-called QDNL Participations fund has a twofold focus: early-stage startups in the sector and research teams working on promising quantum technologies before they incorporate as startups.

In the first case, the funding will reach up to €1.5 million — with the foundation typically leading the investment round. In the second case, the fund will offer €50,000 to researchers via a SAFE note agreement, meaning that the funding will be converted into an equity investment once the startup is ready to progress as a business.

“We get in early and provide objective and patient capital.

The fund expects to make around 10-15 SAFE note investments (of €50,000) and around 5-10 seed investments (of up to €1.5 million), Ton van ‘t Noordende, Managing Director of QDNL Participations, told TNW. “We get in early and we can provide objective and patient capital.”

The fund plans to invest in companies across the quantum sector, including hardware, sensors, entanglement, and superposition technologies, as well as communications and essential supply components.

According to QDNL’s proprietary data, 32.7% of sector funding has gone to software, while 64.4% has been invested in hardware, and almost 3% in hybrid hardware-software.“We expect to follow this trend,” said Van ’t Noordende.

As for the research teams that wish to enter the startup world, they’ll be primarily sourced from leading Dutch universities, including TU Delft, the Eindhoven University of Technology, the University of Tweente, Leiden University, and the University of Amsterdam.

“Spinning out of academia still a bottleneck for European researcher-driven entrepreneurship.

Alongside QDNL Participations, the foundation has also launched a support programme for emerging quantum tech founders, called Infinity. This is designed to help Dutch academic researchers navigate the university spin-out process and raise their first funding round, by providing them access to a network of more than 800 deeptech investors worldwide.

Infinity is offered as an “on-call” service for whenever it might be needed, and is free of charge.

“We believe there’s a massive untapped potential as billions of value in new innovations are left unshared and uncommercialised. Spinning out of academia remains a bottleneck for European researcher-driven entrepreneurship,” Van ‘t Noordende added.

Addressing the funding gap in quantum technology

Fundraising is “the number one challenge” for Dutch deep tech startups, Van ‘t Noordende told TNW. “The [funding] gap does not only exist in the Netherlands, but Europe-wide. Investments raised by US-, UK-, and Canada-headquartered startups account for circa 80% of the value of all private investments in quantum technology and circa 62% of all private rounds.”

As he further explained, the majority of funding “is directed at and above Series A stages,” while multiple factors lead to a lack of an early-stage funding. There’s not only a lack of investors specialised in early-stage investment, but it’s also challenging for investors outside of scientific communities to know “where to invest or how to provide longer term support.”

QDNL Participations aims to address this problem by incorporating a global network of leading quantum tech researchers in the process, who are actively involved in a startup’s early stages, and could later become scientific advisors or board members.

“Our fund removes the risks of what’s seen as a ‘wild bet’ and, through direct intervention, increases the likelihood of long-term impact and financial success,” Van ‘t Noordende added.

According to QDNL’s co-founder and Director of Ecosystem Development Freeke Heijman, the goal of Infinity and the new fund is to enable the sustainable growth of quantum startups in the Netherlands, so they can compete in the global market.

Big business opportunities are brewing in the cosmos. Morgan Stanley predicts the space economy will grow from €355 billion in 2020 to over €1 trillion by 2030 — and competition for the rewards is fierce.

The USA remains a celestial superpower, while China is emerging as a powerful challenger. Europe has historically lagged behind the world leaders — but is now carving out a promising niche.

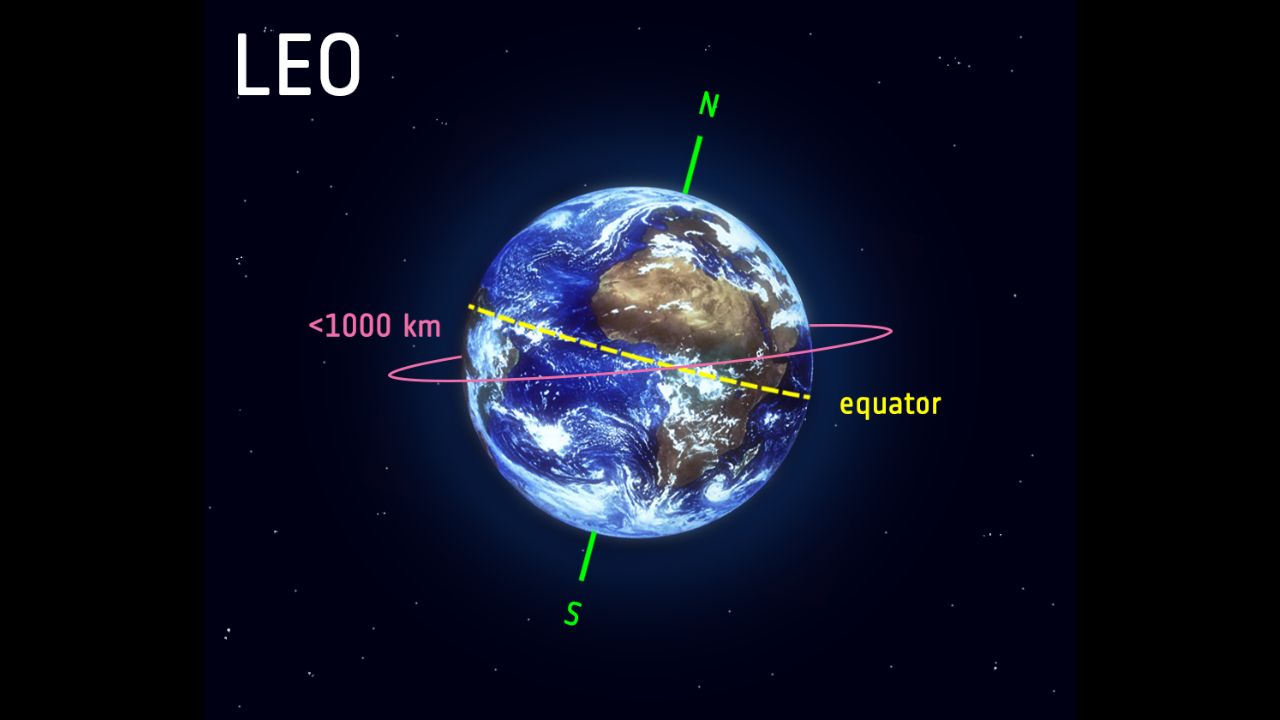

Across the continent, countries are converging around a single segment of the market: small satellites in low-Earth orbit (LEO).

The maximum altitude in LEO is about one-third of Earth’s radius. Credit: ESA

As the name suggests, low-Earth orbits are relatively close to the globe’s surface: a maximum of 2,000km above the planet, and sometimes as low as 160km. Commercial planes, by comparison, rarely fly at altitudes much higher than 14km.

In the 50 years since astronauts last stepped on the Moon, human space exploration has been confined to LEO. Crewless probes still fly deeper into our solar system, but most satellites — as well as the International Space Station — are now found in low-Earth orbit.

The LEO appeal

Small satellites in LEO may lack the glamour of spaceships taking astronauts to the moon, but they offer compelling advantages.

The lower altitude alone has numerous attractions. The costs, risks, and time required for more distant missions have reduced their allure, while the appeal of low-Earth orbit has increased. Among its advantages are speed boosts from gravity’s pull; better signal-to-noise ratios for radar and lidar; higher geospatial position accuracy; expanded launch vehicle options; more convenient journeys and — crucially — fewer resource needs.

‘The pandemic highlighted the need for high-speed connectivity.

Investments have surged as the use cases have expanded. LEO can provide internet connectivity, Earth observation, satellite navigation, and weather forecasting — and it’s becoming more accessible.

As a result, the number of projects in low-Earth Orbit is increasing rapidly. Dan York, who led the Internet Society’s 2022 LEO satellite report, attributes this growth to three key factors: the ceaseless demand for connectivity, the plummeting costs of satellites, and an expanding funding pool.

“The pandemic highlighted the need for high-speed connectivity that can be used for video communication, online learning, e-commerce, and more,” York told TNW. “LEO satellite systems have emerged as a powerful way to provide that high-speed, low-latency connection.”

In the race to commercialise LEO, a single target has been assigned pivotal significance: the first-ever orbital launch from Western Europe.

The territorial advantage

Europe already has a functioning equatorial spaceport — in South America. The Guiana Space Centre in Kourou, French Guiana, has been in operation since 1968. Originally, it served as the spaceport of France, but it’s now shared with the European Space Agency (ESA), which covers two-thirds of its budget.

Despite being 6,000km from mainland Europe, the site has a propitious location. Its position near the equator reduces the energy required for geostationary orbits, which match the rotation of the Earth. Rockets launching east can harness this momentum, while the centre’s proximity to open sea reduces risks to human habitations.

In Western Europe, however, a satellite has still never been sent into orbit — but the milestone is getting closer.

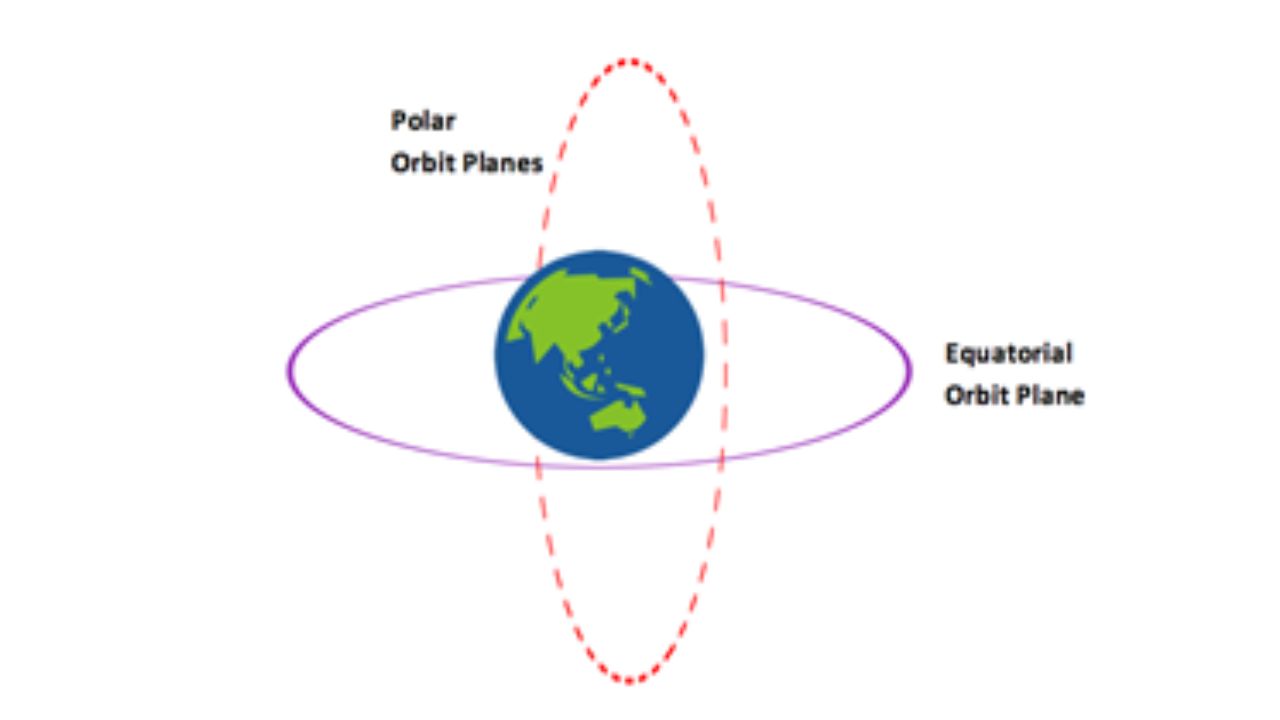

Polar orbits can offer comprehensive views of Earth.

The achievement would provide more mere than bragging rights. A homegrown spaceport would be a powerful launchpad for a budding LEO sector.

The location also has advantages. Western Europe can harness Earth’s rotation to power polar orbits, a flight path that passes the planet from north to south. This trajectory gives satellites extensive views of the planet rotating below, which is particularly useful for observation, mapping, and surveillance.

Further benefits would arise from the proximity to Europe’s production sites, talent, and connected industries.

“For the first time, the EU will have its own telecommunications constellation.

The war in Ukraine has exposed another lure of LEO. As a result of Russia’s full-scale invasion, Ukraine’s terrestrial internet connection has been disrupted by damage, outages, and jamming. In response, Elon Musk’s SpaceX offered free access to the Starlink satellite internet system, which has kept the country connected.

“The success of SpaceX’s Starlink service throughout Europe, and particularly in Ukraine, has shown the power of LEO satellite systems,” said York.

The EU is now developing its own satellite constellation. Known as IRIS2, the network is designed to maintain internet access during crisis situations. The $6.2 billion project is scheduled to launch by 2027.

“For the first time, the European Union will have its own telecommunications constellation, in particular in low orbits, the new frontier for telecommunication satellites,” said MEP Christophe Grudler, rapporteur on the EU secure connectivity programme.

The bloc has grand plans to compete with Starlink — and that’s just one of Europe’s LEO ambitions.

All around the continent, countries are trying to reap the benefits. The first one to reach orbit will get an edge over the competition.

Contenders in the race

Only nine countries and one international organisation (the aforementioned ESA) currently have orbital launch capability, according to the Pentagon.

Booming demand is expected for their services. The number of operational satellites is projected to grow from 5,000 today to 100,000 by 2040 — and spaceports across Europe are sprouting up to launch them.

Among them is a Spaceport Cornwall in the UK. In January, the site tried to send a satellite into orbit, but the attempt ended in bitter disappointment. After the Virgin Orbit rocket was successfully released, an engine malfunction brought the mission to a premature close.

The failure was a painful setback for Britain’s launch sector, but by no means a fatal one. Virgin Orbit is considering another go in Cornwall, while the SaxaVord spaceport in the Shetland Islands is set to attempt a launch before the end of the year. Further sites are under development in Sutherland, Argyll, Prestwick, Snowdonia, and the Outer Hebrides.

Virgin Orbit releases its rockets from a plane, in what’s known as a horizontal launch. Credit: Virgin Orbit

The UK does, however, face growing competition from spaceports in the EU. Most are located in isolated areas of Northern Europe, where populations are sparse and the sea is close.

Sweden’s Spaceport Estrange, for instance, recently became Europe’s first mainland satellite launch facility. The inaugural take-off from the complex is expected in late 2023.

“Europe has its foothold in space and will keep it,” said EU Commission President Ursula von der Leyen at the centre’s opening in January.

Another contender in the race is Andøya Space in Norway, which hopes to launch its first satellite rocket this year. Sites in Iceland, the Azores, Andalusia, the Canary Islands, and the North Sea are also in the running.

“This is exactly the infrastructure we need, not only to continue to innovate but also to explore the final frontier further.” -Ursula von der Leyen, President of the @EU_Commission

“We’re seeing a proliferation of space bases in Europe,” Marie-Anne Clair, head of the Guiana Space Centre, told AFP in December. “The commercial aspect is real: there is also an abundance of micro-satellites which will require missions from micro-launchers.”

An LEO island

A satellite launch provides a springboard for the host nation’s space sector — even if it fails. The UK’s attempt last month, for instance, added impetus to the local industry.

Before malfunctioning, the rocket did reach space, while Spaceport Cornwall became the world’s newest space launch operations centre. The build-up also boosted domestic satellite development and connected an array of talent, businesses, and public sector organisations.

Among them is Open Cosmos, an Oxfordshire-based startup that had a satellite onboard the Virgin Orbit rocket.

“We delivered a satellite in record time,” Open Cosmos CEO Rafel Jordá Siquier told TNW. “It’s sad not to have it in orbit, but we’re ready to come back and rebuild the satellite at an even faster pace if needed.”

Jordá founded Open Cosmos in 2015, with the aims of producing satellite-based solutions for Earth’s biggest problems.

Despite the ill-fated launch, Jordá believes that the UK is now a major player in LEO.

“The UK, with its leadership and its growing commitment towards the space sector, now has a seat at the global table in this industry. And it’s very important that we keep our team there and keep developing our capabilities.”

Those capabilities now encompass downstream applications, data and information services, and the upstream satellite and launch capabilities.

According to Jordá, the UK’s small satellite technology is particularly impressive. Alongside startups such as Open Cosmos, the country is home to OneWeb, one of the world’s leading satellite internet players. In January, the company announced that it now had 542 satellites in orbit – more than 80% of the fleet for its first-generation constellation.

“We now have a truly pan-UK capability.

The landscape also encompasses Surrey Satellite Technologies’ world-leading small satellite platforms, alongside first-rate “CubeSat” nanosatellites produced by Open Cosmos, Clyde Space, and Spire.

Another drawing card is a strong supply chain for space hardware and software. British luminaries in this area range from SMEs such as Teledyne, to aerospace giants like Airbus UK and BAE Systems.

Paul Febvre, CTO at Satellite Applications Catapult and a professor at Bradford University’s new space AI centre, said launch sites will complete the package.

“Now that we are establishing small-satellite launch facilities in both Cornwall and Scotland, with new ventures being developed in East Anglia, we have a truly pan-UK capability which creates the conditions for competition and success,” Febvre told TNW.

The new Bradford-Renduchintala Centre for Space AI plans to launch its own ‘pocket cube’ into LEO in 2024.

Until the British sites are operational, Open Cosmos will take off from other nations. But in the near future, Jordá plans further launches from the UK and France.

“The nice thing about the launch landscape at the moment is that it’s very diverse,” he said. “It’s getting very competitive and that means we have multiple partners that we can work with for different types of orbits.”

Space on the mainland

Another nation with eyes on LEO is France, which has the largest national space programme in Europe.

“France’s space startup ecosystem is particularly strong in LEO satellites, and I think we will see a number of winners emerging from there,” Maureen Haverty, VP at Seraphim, a prolific investor in space tech startups, told TNW.

“France is also the most successful country at encouraging US companies to set up in Europe and is the European hub for a number of key players.”

“We will have our own SpaceX.

A further asset for France is Arianespace, Europe’s leading satellite space launch company. The aerospace giant is currently developing a new reusable rocket, called Maïa, to challenge SpaceX. The launcher is due to be operational by 2026.

“For the first time Europe… will have access to a reusable launcher,” said French Finance Minister Bruno Le Maire last year. “In other words, we will have our SpaceX, we will have our Falcon 9.”

Critics have dismissed the prospect of Maïa competing with SpaceX, but the rocket would at least offer a European alternative. PLD Space in Spain plans to provide another.

The company aims to produce Spain’s first rocket to reach orbit — as well as Europe’s first reusable launch vehicle.

Named Miura 1, the 12.5-meter tall vehicle has a payload capacity of 100kg — just a fraction of the SpaceX Falcon 9’s 25,000kg and the Rocket Lab Electron’s 200–300kg. But PLD Space is confident it can serve the booming demand for small payload launches to LEO.

“We have demonstrated that PLD Space is the most promising company to improve European competitiveness in the microlaunchers race to space,” Ezequiel Sánchez, the company’s executive president, said after a successful test last year.

“This fact makes our project strategic not only for Spain but with a European perspective and a reference to show the profitability of reinforcing investment in new players.”

The public investment in Arianespace provides an edge over rivals that rely on private funding — but the competition is growing.

Smaller startups are also fighting for a spot in low-Earth orbit. Haverty, who oversees Seraphim’s investments in LEO satellite businesses, has seen success from those that tap into domestic expertise.

As an example, she points to Seraphim portfolio company ICEYE, which applies Finland’s strengths in hardware and avionics to world-leading synthetic aperture radar. In Lombardy, meanwhile, D-Orbit has harnessed Italy’s space heritage to establish the planet’s only commercial in-space delivery orbital tug company. The firm recently launched its seventh and eighth missions on SpaceX’s transporter mission.

Prior to joining Seraphim, Haverty was COO at Apollo Fusion, a space startup that was acquired in 2021 for $145M by Astra. She then worked on investments for Astra.

“Overall, I think Europe’s route to success lies in focusing on where they can be world leaders rather than trying to develop a European alternative to an American solution,” said Haverty.

Points of differentiation could also compensate for some shortcomings.

Rejuvenating the old world

The barriers to LEO are lowering, but they remain daunting. Funding in Europe still can’t compete with what’s in the US; space projects are susceptible to delays that can push customers to bigger competitors; nascent markets are tricky to target with commercially viable products.

Startups providing satellite internet services face further obstacles. The established leaders of SpaceX and OneWeb already have LEO constellations in space, customer equipment available, and regulatory approvals in many countries.

“The single biggest challenge for these [European] projects is to get all the components launched and in orbit,” said York, who led the Internet Society’s recent LEO report. “The second biggest challenge is to obtain the regulatory approvals in every country in which they want to operate.”

The growing demand for sparse skills is also difficult to meet. Rewards on offer in the US are often far more lucrative, and the finance and gaming sectors suck up much of the top tech talent.

“We need to encourage and stimulate the understanding in our new generation of engineers, innovators, and entrepreneurs that space is a fantastic place to develop a career and business opportunities, and universities are the knowledge engine for the future economy,” said Febvre, CTO at Satellite Applications Catapult.

At Satellite Applications Catapult, Febvre focuses on growing the UK space industry.

Further problems have emerged in Europe’s commercial launch sector. As well as lacking spaceports, the continent is short on effective rockets. Arianespace’s Vega launcher has been marred by repeated failures, the Araine-5 rocket will soon be retired, and its replacement may not be available for over a year.

The rocket shortage could delay the launch of satellites into LEO. Consequently, Europe has become reliant on commercial launch partners, particularly SpaceX.

“Europe does not have the ‘SpaceX Mafia’ effect.

Haverty adds two further weaknesses compared to the US: a limited product focus in satellite projects and a scarcity of second-generation spacetech founders.

“Europe does not have the ‘SpaceX Mafia’ effect,” she said. “European governments focus more on grants rather than on contracts, which makes it harder to grow startups into big businesses.”

The growing popularity of LEO has created another problem. There’s only so much space in space – and it’s starting to get crowded.

The ESA estimates that there are 36,500 chunks of space debris larger than 10cm, and 130 million between 1mm and 1cm. As these numbers grow, so do the risks of crashes and light pollution.

These threats can also scupper business plans. Regulators consider environmental concerns before deciding whether to allow a satellite launch, but their rules can place heavy burdens on LEO startups. Haverty hopes regulators exert greater pressure on the major operators than their smaller challengers.

“It’s important to remember that the vast majority of debris and causes of potential collisions are caused by the deliberate destruction of satellites by China and Russia,” she said. “Most operators are doing their best to keep space clean.”

On the plus side, the problems of space debris and pollution are presenting business opportunities for space robotics, manufacturing, and in-space servicing. European startups have pitched a range of solutions, from AI monitoring of debris to towing satellites out of LEO.

The ESA and Swiss startup ClearSpace plan to complete the first removal of space debris from orbit in 2025. Credit: ESA

Cleaning up is one of many emerging opportunities in LEO — and Europe is well-poised to grab a share

Despite the challenges, the continent has an enviable array of major satellite operators, affordable engineering talent, a rich history of multinational efforts, and a superlative satellite supply chain.

Insiders hope the spaceport race will further stimulate the sector. The first country across the line may not end up as the best, but the competition can be a boon for all contenders.

The capital flooding into LEO suggests the prospects are strong. Across the continent, investors are betting that a rising tide will lift all spaceships.

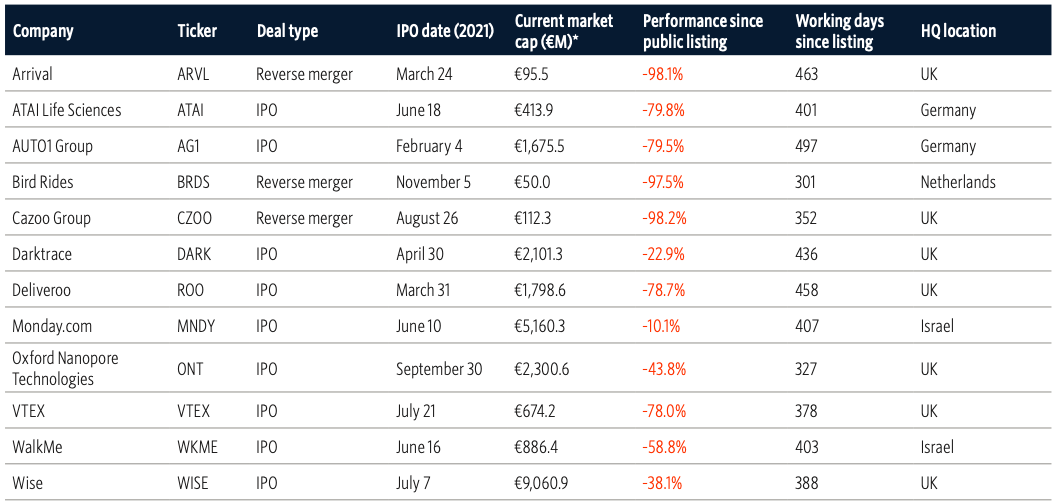

A rough year in public markets has taken a heavy toll on startups. According to new research, every unicorn in Europe that went public in 2021 has since shrunk in valuation.

The losses follow record-highs for VC exit valuations in 2021. PitchBook, a financial data firm, attributed the downturn to a shrinking public market.

The company found that 13 unicorns went public during 2021’s bull market and IPO frenzy. Yet none have gone on to have positive share price returns.

Their numbers paint a gloomy picture. By the end of 2022, more than half of them had lost over 75% of their market cap since going public.

Every European unicorn that had a public listing in 2021. Credit: Pitchbook

Their fortunes have reverberated across Europe’s tech ecosystems. In 2022, there was not a single unicorn exit through a public listing.

“The shutoff of the public listing market plays on the recency bias of founders and their management teams, as they have seen what happened to the companies that went public in 2021,” said PitchBook’s analysts in their latest VC valuations report.

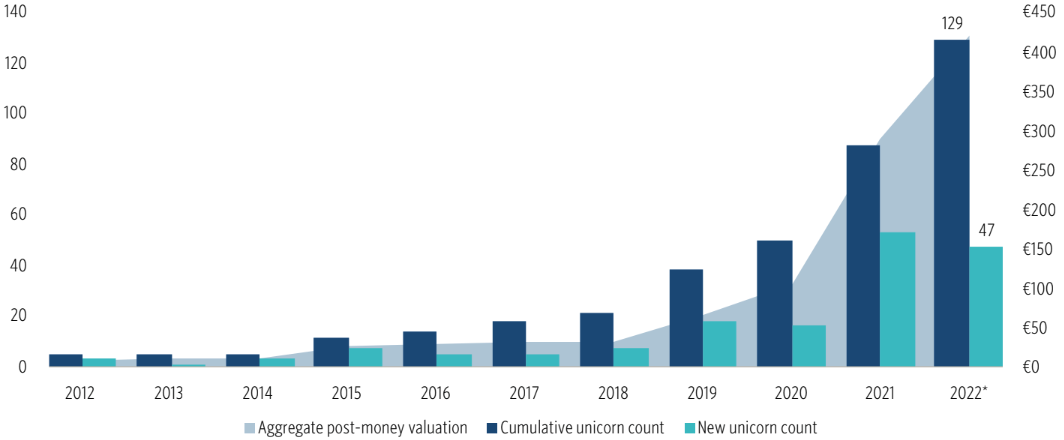

Despite the tough year for exits, there has been positive financial progress for Europe’s leading startups. Last year, 47 new unicorns emerged on the continent —the second-highest figure on record — bringing their cumulative number to 129. Furthermore, aggregate unicorn post-money valuations were increasing dramatically before signs of a slowdown emerged. Yet the newest members of the herd are electing to stay private.

New and cumulative unicorn count and aggregate post-money valuation (€B). Credit: Pitchbook

Notably, food delivery startups had impressive exits via acquisition in 2022. Finland’s Wolt was bought by DoorDash for €2.7 billion, Spain’s Glovo was acquired by Delivery Hero for €800 million, and Germany’s Gorillas was snapped up by Getir for €1.2 billion.

These exit routes, however, may prove to be anomalies. According to Pitchbook, most unicorns now prefer to remain within the VC ecosystem.

Get the TNW newsletter

Get the most important tech news in your inbox each week.