Munich-based autonomous trucking startup Fernride has closed a further $19mn in its Series A funding round, neatly pushing the total amount raised in the round to $50mn.

Founded in 2019, Fernride has developed autonomous vehicle software that converts trucks into self-driving machines. These haulers operate at Level 4 autonomy which means the vehicle can drive itself within a specific area — albeit with a bit of supervision from a remote driver.

There is a current shortage of 400,000 truck drivers in Europe — a figure projected to increase to two million by 2026. Despite autonomous driving being a potential solution to these challenges, many attempts to introduce such autonomy fail, partly due to regulatory roadblocks.

A spin-off from the Technical University of Munich, Fernride bypasses some of the red tape hindering other self-driving car companies by focusing (for now) on trucks for private industrial sites like factories, terminals, and shipyards. This allows the company to scale its product now, and tackle the multiplicity of problems associated with deploying autonomous vehicles on public roads later.

Fernride is currently working with four big names, including Volkswagen’s logistics unit and DB Schenker, part of the German rail group Deutsche Bahn. It currently has a fleet of six autonomous trucks with plans to scale to 20 by the end of 2023. These yard trucks are limited to 30 kmph, and stop to call a remote operator if they don’t “understand” a situation. Fernride trains a remote operator on every site where its trucks are deployed.

The trucks are supervised by a so-called teleoperator. Credit: Fernride

New investors include Germany’s DeepTech and Climate Fonds (DTCF) and the ERP special fund, as well as Munich Re Ventures, Bayern Kapital, and Klaus Kleinfeld, who becomes chair of Fernride’s board.

“By starting with teleoperations that initially keeps a human in the loop, we believe Fernride’s step-by-step approach is the optimal path towards building fully autonomous capabilities,” said Timur Davis, director at Munich Re Ventures.

Armed with fresh funds, the startup now looks to scale operations with its existing customers (which alone have a combined 1,000 yard trucks suitable for automation). Fernride also looks to explore new customers and markets, with plans to expand to the US sometime in 2025.

When it comes to saving the world — or, let’s face it, civilisation, the planet will recover — there is no silver bullet. Rather, it is going to take a holistic approach of caring for the Earth and each other.

A technological revolution got us into this pickle. Ironically, technology might just be the Hail Mary that will pull us, if not entirely out of it, then at least away from the brink of total disaster. But in order for that to happen, it is us humans who need to set our minds — and money — to it.

Recently launched venture capital firm Transition wants to support emerging technologies looking to help our planet. This includes, but is not exclusive to, reducing carbon emissions. Based out of London with offices in Reykjavik and New York, the climate tech VC is the brainchild of a group of experienced funders who saw a tremendous gap between early stage and later stage funding in the sector.

“What we saw was that there was this real gap in the market where there was a lot of activity at angel stage and seed stage. And then there is an enormous amount of capital available for later stage investing, which will only grow due to climate-focused targets,” Kristian Branaes, one of Transition’s partners, previously with CPP Investments and Atomico, told TNW.

The <3 of EU tech

The latest rumblings from the EU tech scene, a story from our wise ol’ founder Boris, and some questionable AI art. It’s free, every week, in your inbox. Sign up now!

“But there are actually very few companies that make it out from all the great accelerators and incubators that exist, and very few that can absorb a lot of capital,” Branaes added, referring to an increasing interest from very large organisations, such as pension funds, to invest more in clean and climate tech. This means that a lot of technology currently being developed risks being left behind.

Indeed, data supports Branaes’ and his partners’ observations. A report published by Economist Impact last week found that, in 2021, only 6% of private investment in the sector went to emerging or early-adoption technologies. The remaining 94% was directed towards more mature tech, such as EVs, energy storage, and solar power.

Climate tech lost in translation

The relationship between equity investing and climate tech is an inherently complicated one. The two sectors, finance and science/engineering, not only have a different vocabulary but also work according to very different time horizons. To function well together, the funding side will need to get comfortable with different measures of success and potentially new revenue models. Meanwhile, scientist-founders need to find ways of translating innovation to commercialisation and business plans.

“We see a lot of scientists coming out of PhD or postdoc, towards the beginning of their academic professional career, that have been very much focused on one topic, or a very narrow scope, and completely understand that topic,” said Transition Venture Partner Bruis Van Vlijmen. The key to the “translation puzzle,” he states, is to be able to look up and see the complete picture.

And Van Vlijmen should know. He has trained on traditional thermo-mechanical storage systems at TU Delft in the Netherlands, and worked on ocean wave energy generation at UC Berkeley and energy storage solutions at Stanford, before becoming involved in the VC/startup ecosystem in the SF Bay Area.

“That translation [between science and business], I think, really comes from being able to kind of download all the scientific knowledge from the depths of your understanding to something like a common playing field and an economic framework that everyone can understand.”

In service of planetary life-support systems

Transition began raising funds in June 2022 (according to a Securities and Exchange filing amounting to $200mn). The firm focuses specifically on companies that will help restore/improve/reduce human detrimental impact on one of the “planetary boundaries.”

These were defined by a group of researchers in 2009, and are processes that regulate the stability and resilience of the Earth’s system at risk due to human activity — including climate, biodiversity, and land system change.

Exceeding the safe operation within these boundaries could, the researchers argued, “be deleterious or even catastrophic due to the risk of crossing thresholds that will trigger non-linear, abrupt environmental change within continental- to planetary-scale systems.”

In an update to the study published in Nature earlier this year, scientists found that humans have surpassed seven out of eight boundaries.

“We think of climate in a slightly broader way, rather than just focusing on, say, a specific CO2 cutoff point,” Branaes said. “And that’s because what matters to us is having a livable prosperous planet for all of us to enjoy.”

Unlocking the business side of innovation

This broader impact strategy is evident in the startups that Transition has chosen to back this far. Among them are Waterplan, which develops software for enterprises to measure, respond, and report on increasingly changing water risk. Others are plant-based plastics developer FabricNano, and SixWheel, which offers a swappable battery solution and charging network for trucks.

Another still is Phase Biolabs based out of Nottingham, UK, for which Transition led the seed round in 2022. The company uses a gas fermentation process where captured CO2 is introduced into a tank where it is “eaten” by patented microbes, which produces chemicals and fuels, similar to the process of making wine or beer.

“The biggest thing Transition has done for us is reinforce some of the key things that you need to kind of figure out or unlock on the business side of establishing a new company,” said David Ortega, founder, CEO and CTO, of Phase Biolabs.

“Because of their diverse and experienced team, they have been able to provide that guidance that someone like me, who lacks that experience, needs to try and make fewer mistakes,” Ortega continued, adding how important it is for scientists to learn how to translate their technology into a value proposition.

Along with Branaes, Transition’s other partners are Mona Alsubaei (formerly with Union Square Ventures), David Helgason (founder of Unity Technologies), and Ari Helgasson (previously an investor at Index Ventures and Dawn Capital, and co-founder of Uphance and ecommerce startup Fabricly).

There may not be one single solution that will solve the challenges we collectively face. However, as a Swedish saying goes, “small streams make great rivers.” If all the amazing innovation that exists and is yet to be discovered out there receives the right level of support, we may just stand a chance.

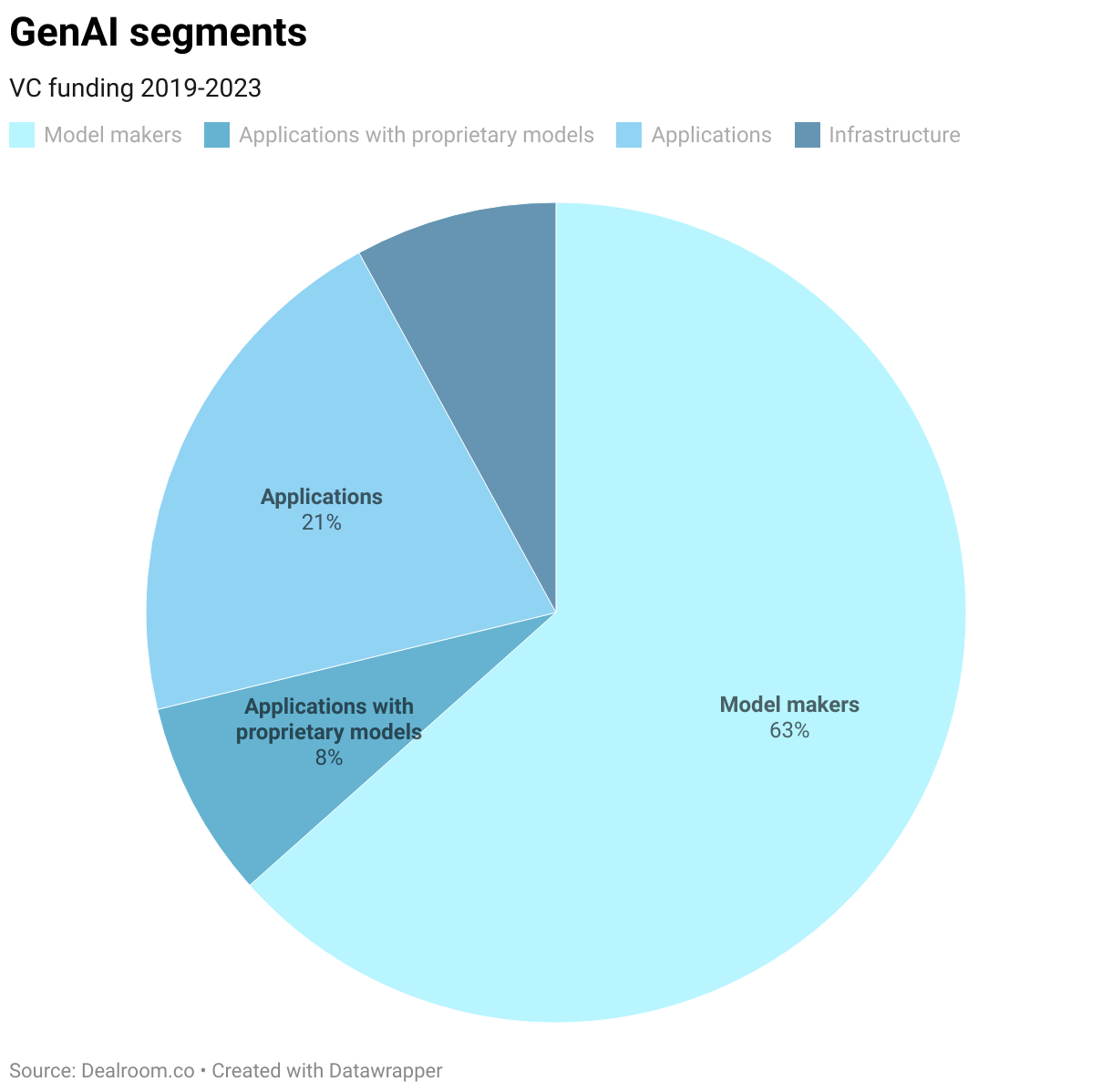

European startups got just $1bn of the €22bn that VCs have invested in generative AI since 2019, according to data from Dealroom.

Unsurprisingly, American companies attracted the bulk of the money. A whopping $20bn — 89% of the global total — went to US startups. Their Asian counterparts raised only $790mn, while the rest of the world combined bagged just $454mn. Dealroom’s data collection ended on July 10, 2023.

US startups have raised 89% of globally GenAI investment 😳

In the last decade, venture capital has gone global. More than half of VC investment is now raised outside the US. Not so in Generative AI.

The US dominance is partly explained by the rise of OpenAI. The company has been a VC darling since the launch of ChatGPT, which sparked the generative AI boom. Venture capitalists ploughed nearly $12bn into the San Francisco-based company.

OpenAI is also the leading name in Dealroom’s model maker segment, which accounts for over 60% of the total VC funding for GenAI. Other big players in the field include Anthropic, Adept AI, Inflection AI, and Aleph Alpha. The next most funded segments are applications and infrastructure.

The Bay Area, where OpenAI is based, has become the epicentre of generative AI. VCs funnelled over $18bn into startups in the region. The next leading cities in the sector were New York ($676mn) and Tel Aviv ($433mn).

Outside of the top three, the landscape is a lot brighter for Europe.

London took fourth place in the rankings. GenAI startups in the UK capital raised around $36mn, led by the $101mn investment in Stability AI, which makes the Stable Diffusion text-to-image model. Three European cities rounded out the top 10: Berlin ($141mn), Amsterdam ($238mn), and Stockholm ($100mn).

Get the TNW newsletter

Get the most important tech news in your inbox each week.

Yesterday we reported that UK chip design company Arm was valued at just above $50bn before going public on the Nasdaq stock exchange. At the end of the day, the share price had jumped by close to 25% above the debut price. It rose from $56.10 to $63.59 — much higher than the $51 presented on Wednesday.

This made it the largest public listing in the US in nearly two years. The significant jump in share price could be attributed to the fact that the IPO was oversubscribed by up to 10 times. As a result, banks had closed their order books one day early on Tuesday.

Arm doesn’t produce or sell actual computer chips. Rather, it designs their blueprints and then sells those along with the intellectual property and instruction sets. This approach has earned it a unique and essential role in the semiconductor supply chain. Strategic investors in the IPO include some of Arm’s biggest customers — Nvidia, Intel, Apple, Samsung, and TSMC.

According to Bloomberg, in a final push before trading commenced, some bankers wanted to price the share above marketed range. However, SoftBank chairman and CEO Masayoshi held his ground, stating it wasn’t worth risking a healthy debut for $100mn or so in additional proceeds. It turned out to be a successful strategy — Thursday’s IPO raised $4.87bn for SoftBank, which shelled out $32bn when it first bought Cambridge-based Arm in 2016.

The upped valuation is in line with an internal transaction last month. This saw the Japanese conglomerate buy back 25% of the company from Saudi-backed investment vehicle Vision Fund (managed by SoftBank itself). Vision Fund lost a staggering $30bn last year after betting on an array of unsuccessful startups. It laid off dozens of employees as a result, but managed to turn a profit again last quarter, due to a rally in tech stock performance.

Having firmly established itself as an essential part of the smartphone value chain, Arm will now look to grow, and potentially make itself equally indispensable, in the automotive, data centre, and AI sectors. With these markets’ seemingly insatiable appetite for chips, it would appear the sky’s the limit for those who found themselves with newly offered Arm shares.

That being said, potential clouds of concern could be gathering due to its dependence on China (the country accounts for a quarter of Arm’s sales) coupled with tension in trade relations and export restrictions. Furthermore, it will have to contend with the rising challenge from open source instruction set architecture RISC-V. Time will tell.

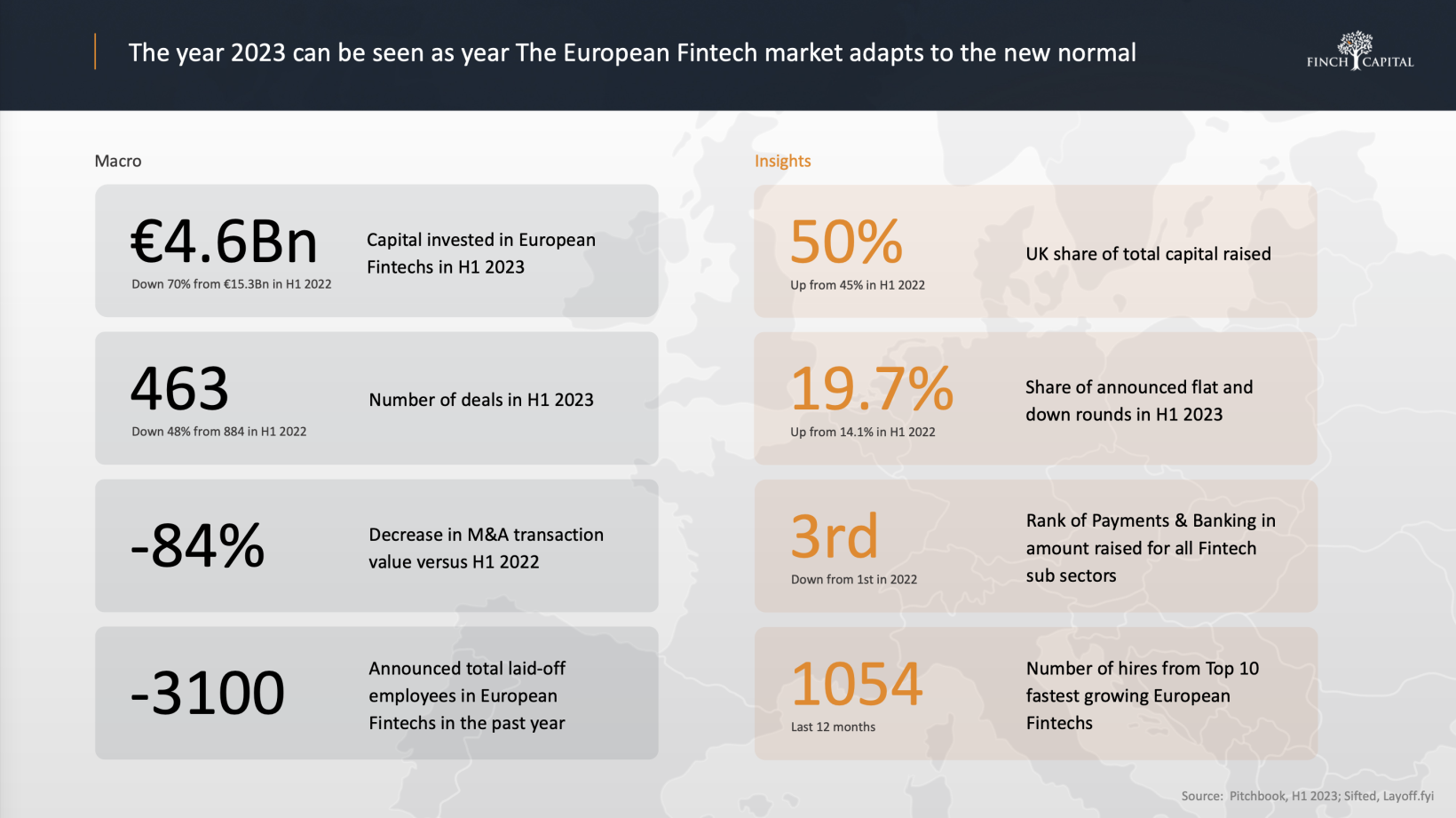

Fintech funding in Europe has been greatly affected by the challenging economic environment, the latest report by Finch Capital has found. Specifically, startups in the sector raised a total of €4.6bn in the first half of 2023 — down 70% from €15.3bn in H1 2022.

“Since mid-2022 we have seen an increase in investment discipline in public and private markets, resulting in less funding, lay-offs, less IPOs, flight to quality, and focus on capital efficiency,” said Radboud Vlaar, Managing Partner at Finch Capital.

Amid this increased funding discipline, this year’s first half has seen a 48% decline in the number of deals (434 in total) alongside an 84% decrease in M&A transaction sizes, compared to the equivalent 2022 levels. On the bright side, overall M&A activity fell only by 5% with volumes to match those of the past year.

Meanwhile, although the top 20 funding rounds are back to pre-2020 levels, investment dropped the most for the rest, which accounted for less than 40% of the total deal volume. Startups in the Series A to C stages have felt the heaviest impact. In contrast, seed rounds continued to attract funding.

Credit: Finch Capital

The <3 of EU tech

The latest rumblings from the EU tech scene, a story from our wise ol’ founder Boris, and some questionable AI art. It’s free, every week, in your inbox. Sign up now!

From a valuation perspective, public markets have withdrawn to 2019 levels, after record growth in 2020-2021, but are showing signs of stabilisation. Private markets are also transitioning to 2019 valuation levels at a comparable but slower pace.

“We should also start to see a slow recovery of the IPO market in the next semester as valuations have started to slowly pick up and inflation is declining,” noted Vlaar.

Crypto on the rise

Crypto and Lending have attracted most of the investments, displacing Payments and Banking — a traditionally resilient category that saw record capital deployed in 2022. Notably, one in three fintech startups are now labelled as crypto/blockchain.

From B2C to B2B

The report has also found that the trend of the past years towards B2B fintech is here to stay. One reason why is the growing interest in regulation technology as payments and open banking are increasingly consolidating. Another is generative AI’s potential applications in retail banking and the insurance sector.

The UK leads in funding

A well-established fintech hotspot, the UK has shown more resilience and accounted for over 50% of the funding in Europe.

Nevertheless, the UK, Germany, and France also saw a 70% decline in funding value, but optimistically, exits continued consistently. Poland recorded the biggest drop at 89.9%. Overall, countries with an active Series A-B investor base, have seen valuations hold up with small increases in post-money valuations.

The “new normal”

“Consolidation and more competitive investment flows, combined with still significant levels of undeployed capital, will bring maturity to the fintech sector. This new normal level of activity demonstrates the refocus of the fintech ecosystem on long term sustainability versus short term gains,” said Vlaar.

And although the overall environment will continue to be challenging in the next 12 months, he added that this will result in “a more healthy and sustainable startup, hiring, and investor ecosystem.”

Today, the Saïd Business School at the University of Oxford, along with early-stage VC OpenOcean, released what they call “the world’s most accurate open access startup insights platform” — the O3.

The platform is the result of three years of research from Oxford Saïd and 13 years of experience of data economy investing from OpenOcean. It leverages public and private data sources and is meant to help improve decision making across the UK tech ecosystem, through “granular data on startups and their technology stack, solutions, and go-to-market strategies.”

“In my time in venture capital, far too often the choice of which startups receive funding has come down to instinct and opportunistic use of data, rather than accurate definition and comparison of startups,” said Ekaterina Almasque, General Partner at OpenOcean. “We wanted to change that, creating a platform that cuts through the noise, and removes bias from decision-making.”

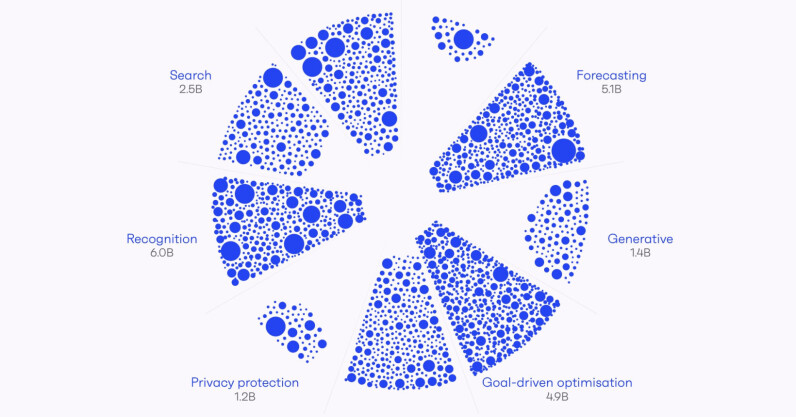

The O3 platform has already screened 16,913 UK startups according to a unique taxonomy developed by Oxford Saïd. For an initial analysis, it has looked specifically at high-growth startups that use or facilitate AI (close to 1,300), and has come up with some interesting findings about the sector.

AI startups a small portion of UK tech ecosystem

The <3 of EU tech

The latest rumblings from the EU tech scene, a story from our wise ol’ founder Boris, and some questionable AI art. It’s free, every week, in your inbox. Sign up now!

The UK government has asserted that it is going to make the country an AI powerhouse. However, thus far, the number of UK startups with a pronounced AI focus make up less than 10% of the ecosystem.

Mari Sako, Professor of Management Studies at Oxford Saïd, believes that the O3 will enable policymakers, researchers, founders, and investors to clearly identify gaps and opportunities in the AI ecosystem. “We believe this platform has immense potential to aid innovators in making informed decisions based on sound data, and to boost research on AI,” Sako said.

UK fintech is generally a top investment destination in Europe, but when it comes to AI, the health tech startup segment receives more funding (£2.6bn vs. £3.4bn, respectively).

Startups using AI for recognition tasks, including but not exclusive to facial recognition, have collectively raised the most funding (£6bn). Meanwhile, among the least funded are those focusing on privacy protection (£1.2bn).

The analysis has also uncovered, perhaps unsurprisingly, a significant bias towards London for startup fundraising. However, there is also notable support in Bristol, Oxford, and Cambridge.

According to the originators of the platform, the UK is only the beginning. “We want to see it expand to cover more markets and geographies,” Almasque continued. “It is a community driven project, built on open access, where the more stakeholders participate, the more powerful is the common knowledge.”

NordicNinja, the largest Japanese VC in Europe, has raised a fresh fund of €200mn for early-stage startups active in climate and deep tech, with particular focus on the intersection between sustainability and digitalisation.

Alongside the funding, startups will receive support and access to a network of over 120 blue chip Japanese corporations.

Founded in 2019, NordicNinja is led by a team of founders, engineers, and operators turned investors from Northern Europe and Japan. While the firm’s focal point has been so far on the Nordics and the Baltics, it’s now expanding to the UK, Ireland, and BeNeLux countries. Its headquarters are in Helsinki.

NordicNinja’s first €110mn fund was invested in a total of 20 companies, three of which have achieved unicorn status: Sweden-based Einride and Voi and Estonian Bolt. Overall, the VC funded technologies ranging from self-driving electric trucks and climate action toolkits for cities, to AI identity verification and mixed reality headsets for astronauts.

According to the company, the second fund will continue targeting climate and deep tech startups whose founders are driving sustainability and digital transformation forward. Its biggest investor is Japan Bank of International Cooperation (JBIC), while it’s also backed by Japanese Honda and Omron, and a number of European investors including BaltCap and Swedbank pension funds.

“Thousands of kilometres apart, Japan and Europe have much in common. Both have company-building legacies, an appetite for innovation, and understanding of the need to take care of the planet,” said Tomosaku Sohara, Managing Partner at the VC.

“NordicNinja is a bridge that turns these shared interests into common goals, bringing two of the world’s biggest ecosystems together for the benefit of us all.”

Space startup Open Cosmos will accelerate its mission to protect our planet after raising $50mn in a new funding round.

The UK-based company uses satellites to tackle environmental issues. By tapping AI, sensors, and Earth Observation (EO) imagery, the probes provide unique insights into climate change.

These findings can shine new light on global temperatures, greenhouse gases, polar ice caps, sea level changes, natural disasters, and deforestation. Scientists can then use the data in damage mitigation programmes.

Rafel Jordá Siquier, Open Cosmos’ CEO and founder, told TNW that sustainability is at the core of the company.

The <3 of EU tech

The latest rumblings from the EU tech scene, a story from our wise ol’ founder Boris, and some questionable AI art. It’s free, every week, in your inbox. Sign up now!

“I’ve always believed that space data holds the key to building a more resilient and sustainable world enabling us to better understand, predict and react to different challenges and make informed decisions,” he said.

“These detailed global views, combined with advanced data visualisation tools, provide organisations all around the world with the insights they need to make changes that, in time, will better protect our planet.”

Rafel Jorda Siquier, Open Cosmos founder and CEO. Credit: Open Cosmos

Among the current crop of Open Cosmos satellites is Menut, which launched in January aboard a SpaceX Falcon 9 rocket. The nanosatellite was built to monitor deforestation, wildfire impact, flooding, and coastal erosion.

If all goes to plan, Menut will soon have several new colleagues in space. By March 2024, Open Cosmos plans to launch the following five satellites:

PLATERO, which will monitor the environmental impact of farming in Andalusia.

IOD6, which will use hyperspectral imagery to survey Atlantic coastal and maritime areas.

MANTIS, which will produce high-resolution images of logistics, energy infrastructure, and natural resources.

ALISIO1, which will make environmental observations in the Canary Islands for applications including agriculture and disaster management.

PHISAT2, a cubesat with six onboard AI applications that will process data in orbit.

To maximise the benefits, the satellites can connect to the OpenConstellation, which organisations use to share and access space data.

Menut, which is Catalan for “small” will orbit around 538km from the Earth at a speed of about 8 km/s. Credit: Open Cosmos

OpenConstellation is part of an end-to-end service, which covers the design, build, and operation of satellites. According to Open Cosmos, the model democratises access to space by cutting costs and simplifying processes.

“The space sector has traditionally been seen as quite an exclusive one,” Jordá said. “It’s expensive to build and design satellites, costly to access and use them, and you also need a high-level science and tech understanding to leverage the tools.

“This is why ensuring access to space data is so important and why the space sector should prioritise this because this bridges the gap between upstream and downstream, as this is where the most growth will come from.”

Research suggests that they could also reap financial benefits. Last year, analysts predicted that the EO satellite market would be worth $11.3 billion by 2031.

To maximise the potential, Jordá wants stronger backing from the public sector.

“Particularly in the UK, we need government-funded projects to allow us to continue to fuel this rich innovation we’re seeing and support companies to go from concept to commercialisation,” he said.

Our world runs on semiconductors. The slivers of silicon provide electronic brains to phones, computers, cars, data centres, and stock markets. They’re also the digital backbone of modern militaries.

Some of the first chips ever made were used in missile guidance systems. Today, they power countless military devices, from fighter jets and howitzers to radios and radar.

In the Russian-Ukraine war, chips power HIMARS rocket launchers, Javelin anti-tank missiles, and the Starlink communications satellites. They’re also integral to the arms race underway in East Asia, where territorial disputes in the East and South China Seas risk spiralling into a major conflict. The rise of artificial intelligence adds another dimension to the tensions: there’s now a dearth of AI chips.

In the EU, the shortages and frictions have led the bloc to introduce the €43bn Chips Act. The investment package aims to boost local production and reduce international dependencies. Experts, however, have downplayed any prospects of sovereignty.

According to Chris Miller, the author of Chip War, the EU has “no chance” of semiconductor independence — and neither does anybody else.

The <3 of EU tech

The latest rumblings from the EU tech scene, a story from our wise ol’ founder Boris, and some questionable AI art. It’s free, every week, in your inbox. Sign up now!

The problem, he argues, is that the supply chain is simply too globalised and interconnected.

“Independence is hopeless,” Miller, an economic historian, told TNW at the IFA Berlin tech show. “It’s not going to happen — nor do I think Europe is pushing for it.”

A divided industry

In Chip War, Miller recounts the decades-long battle to control semiconductors, which today centres on the rivalry between the US and China. Tensions between the nations have torn the chip world into two.

As the fractures widen, Beijing is trying to bolster self-sufficiency in semiconductors. It’s currently the world’s largest importer of the devices, spending more money importing them than it does on oil.

Miller is currently a history professor at Tufts University and a visiting fellow at the American Enterprise Institute. Credit: Chris Miller

To constrain China’s ambitions, Washington has imposed sweeping export controls on chip tech. In 2022, the Biden administration imposed its toughest sanctions yet. Under the new rules, the White House could block not only sales of chips made in the US, but also chips that use American components or software.

The move has disrupted China’s trade with Taiwan, which produces over 60% of the world’s semiconductors — and over 90% of the most advanced ones.

Beijing has also encountered problems in the EU, which has its own chip powerhouse: ASML.

The Dutch company is the world’s leading manufacturer of high-end chipmaking equipment. Without its gear, Chinese firms will struggle to produce advanced chips.

That outcome could soon become a reality.

Europe’s chip future

Amid pressure from the US, the Netherlands began restricting exports of advanced chip manufacturing equipment on September 1.

The move has sparked fears that China will impose retaliatory restrictions. Miller, however, expects Beijing to proceed with caution. He notes that retaliation could backfire.

“China could cause disruptions in supply chains, but they could be just as impacted by the disruptions as the West is,” he said.

Nonetheless, the discord has amplified calls for autonomy. In response, the EU has made plans to produce 20% of the world’s semiconductors — double its current share — by 2030.

It’s a target that Miller believes is “possible,” but only with strong support from the member states and companies.

A precedent for this approach has been set this year in Germany. After offers of enormous subsidies, both Intel and Taiwan’s TSMC have pledged to build chip factories in the country.

Ultimately, semiconductor independence may be impossible — but the EU already has some unique strengths. In machine tools and power semiconductors, for instance, the bloc is home to some of the world leaders.

“I think Europe should keep focusing on what it’s historically been very good at, which is investing in R&D-intensive manufacturing industries,” said Miller.

“The goal is to have profitable chip companies with technological leadership positions — and Europe has that.”

Intel Ignite, Intel’s accelerator for early-stage deep tech startups, has unveiled the 10 companies that will comprise its newly-launched London cohort — the first one in the UK.

Starting on September 12, the selected startups will take part in a 12-week programme, during which founders will receive mentorship and guidance on their growth journey. This will include areas such as product development, technology, marketing and sales, fundraising, and go-to-market strategies.

The programme will also focus on co-founder dynamics, founders’ mental health, and diversity and inclusion practices.

Meanwhile, the finalists (selected from a total of over 200 applicants) will have access to a funding pool of $7.6mn (€7.1mn), provided by external investors. The startups themselves will pay no participation fees.

The 10 companies represent multiple sectors of deep tech, ranging from generative AI, machine learning, and next-gen computing to robotics and manufacturing.

Here’s the full list:

Apoha: sensory intelligence to anchor machines into physical reality.

Circuit Mind: electronics design assistant for engineering teams.

Crypto Quantique: chip-to-cloud system to manage and secure IoT devices in a single platform.

Fianchetto: light-speed photonic processors for faster and more sustainable computing.

Ivy: unifying all AI frameworks, hardware, and infrastructure with one line of code.

LGN: edge AI management software for businesses.

Lumai: scalable and ultra fast 3D optical interference processor.

VyperCore: acceleration and protection of computer-intensive applications via novel microprocessor design.

“With these pioneering startups, Intel Ignite is thrilled to be launching the first cohort in London, which is home to the third-largest market in the world of startups and the number one market outside of the U.S.,” said Tzahi Weisfeld, Intel’s VP and general manager of Intel Ignite.

Intel Ignite was launched in 2019 and counts three more hubs across the globe: Munich, Boston, and Tel-Aviv. So far, a total of 148 companies have participated in its accelerator programmes, having raised a total of $1.7bn (€1.6bn) in funding.

Deep tech startups interested in participating in the next London cohort can submit their application at the Intel Ignite website.

Estonian startup VOOL has secured a fresh capital injection of €2.92mn to boost production and development of its EV charging solutions. Specifically, the company closed an additional seed round of €1.3mn and received a €1.6mn grant from the Estonian government.

Founded in 2018, VOOL offers a smart EV charging system, which combines in-house developed hardware and software. This includes the charger, hub, app (B2C), web platform, and admin portal (B2B).

VOOL’s EV charger is suitable for both businesses and private customers. Credit: VOOL

The company claims its solution uses the existing grid three times more efficiently than average thanks to its “three-phase” technology.

“Currently, you still have access to only a fraction of the full capacity of the grid, even though the whole of Europe is connected to three phases of electricity,” explains the co-founder and CEO of VOOL, Juhan Härm. “We use all three phases and automatically switch between them when needed. This way, we can offer reliable and sustainable automatic charging,” he adds.

The startup employees 44 people. Credit: VOOL

The <3 of EU tech

The latest rumblings from the EU tech scene, a story from our wise ol’ founder Boris, and some questionable AI art. It’s free, every week, in your inbox. Sign up now!

VOOL’s software also tracks electricity prices to make sure the EV is charged at the lowest cost possible within the set timeframe, which, according to Härm, enables users to save up to 90% on charging costs.

The new capital has a threefold aim: to scale up the recently-launched charger production; to grow the international sales and customer support team in the Nordics; and to develop new household products for grid optimisation.

The seed funding round was led by Specialist VC, investment company Amalfi, and a mix of real estate developers.

VOOL also secured capital from new angel investors, including Taavi Veskimägi, the former chairman of the board of Estonia’s independent electricity and gas system operator Elering. Notably, however, the biggest angel investors were the startup’s own employees, accounting for 15% of the investment.

The company’s total funding now stands at €7.62mn.

When Russian troops flooded into Ukraine last year, an army of propagandists followed them. Within hours, Kremlin-backed media were reporting that President Zelenskyy had fled the country. Weeks later, a fake video of Zelenskyy purportedly surrendering went viral. But almost as soon as they emerged, the lies were disproven.

Government campaigns had prepared Ukrainians for digital disinformation. When the crude deepfake appeared, the clip was quickly debunked, removed from social media platforms, and disproven by Zelenskyy in a genuine video.

The incident became a symbol of the wider information war. Analysts had expected Russia’s propaganda weapons to wreak havoc, but Ukraine was learning to disarm them. Those lessons are now fostering a new sector for startups: counter-disinformation.

Experts feared the Zelenskyy deepfake was merely the tip of the iceberg, but the iceberg is yet to emerge.

Like much of Ukrainian society, the country’s tech workers has adopted aspects of military ethos. Some have enlisted in the IT Army of volunteer hackers or applied their skills to defence technologies. Others have joined the information war.

In the latter group are the women who founded Dattalion. A portmanteau of data and battalion, the project provides the world’s largest free and independent open-source database of photo and video footage from the war. All media is classified as official, trusted, or not verified. By preserving and authenticating the material, the platform aims to disprove false narratives and propaganda.

Dattalion’s data collection team leader, Olha Lykova, was an early member of the team. She joined as the fighting reached the outskirts of her hometown of Kyiv.

“We started to collect data from open sources in Ukraine, because there were no international reporters and international press at the time,” Lykova, 25, told TNW in a video call. “In the news, it was not possible to see the reality of what was happening in Ukraine.”

In addition to her role at Dattalion, Lykova works in project management for Luxoft Ukraine.

Since the project was established on February 27, 2022 — just three days after the full-scale invasion began — Dattalion has been cited in more than 250 international media outlets, from NBC News to Time. With the mooted addition of a paid subscription service, it could also be monetised — a thorny challenge for the sector.

An emerging sector

Counter-disinformation is not an obvious magnet for consumer cash. Nonetheless, the sector is attracting unusual investor interest.

Governments are particularly enthusiastic backers.In the US, more than $1bn of annual public funding is allocated to fighting disinformation, the Department of State said in 2018.Across the Atlantic, European nations are investing in targeted initiatives. The UK, for instance, created a ‘fake news fund’ for Eastern Europe, while the EU has financed AI-powered anti-disinformation projects.

Big tech is also writing big cheques. Since 2016, Meta alone has ploughed over $100mn into programs supporting its fact-checking efforts. In addition, the social media giant has splashed cash on startups in the space. In 2018, the companyspent up to $30mn to buy London-based Bloomsbury AI, with the aim of deploying the acquisition against fake news.

Still, not every tech giant is enthusiastic about corroborating content. Under Elon Musk’s leadership, X (formerly Twitter) has dismantled moderation teams, policies, and features. The approach has been praised by fans of Musk — a self-proclaimed “free speech absolutist” — but triggered spikes in falsehoods on the app.

Alarmed by the controversies, brands have fled the platform in their droves. In July, Musk said X had lost almost half its ad revenue since he bought the company for $44bn last October.

According to a new EU study “the dismantling of Twitter’s safety standards” boosted “the reach and influence of Kremlin-backed accounts.” Credit: Daniel Oberhaus

As X grapples with the concerns of advertisers, a wave of tech firms are offering solutions. In the last couple of years, over $300mn has been ploughed into startups that tackle false information, according to Crunchbase data. Two of them have raised over $100mn each: San Francisco-based Primer and Tel Aviv’s ActiveFace. Both companies develop AI tools that can identify disinformation campaigns.

Ukrainian startups are also starting to raise funding— and there are signs that the investments could soon surge.

“Ukraine has been waging an informational struggle for more than 10 years.

In the EU, tech companies now have to comply with the Digital Services Act (DSA), which requires platforms to tackle disinformation. If they don’t, they face fines of up to 6% of their annual global revenue.

X’s DSA obligations have received particular attention. In June, the company received the first “stress test” of the regulatory requirements. After the mock exercise, Musk and Twitter CEO Linda Yaccarino met with EU Commissioner Thierry Breton, who oversees digital policy in the bloc. Breton emphasised a threat that Ukraine recognises all too well.

“I told Elon Musk and Linda Yaccarino that Twitter should be very diligent in preparing to tackle illegal content in the European Union,” he said. “Fighting disinformation, including pro-Russian propaganda, will also be a focus area in particular as we are entering a period of elections in Europe.”

A brief history of the disinformation war

Since the early Soviet Union, Russia has been a pioneer in influence operations. Historians have traced the very word “disinformation” to the Russian neologism “dezinformatsiya.” Some contend that it emerged in the 1920s, as the name for a bureau tasked with deceiving enemies and influencing public opinion.

Defector Ion Mihai Pacepa claimed the term was coined by none other than Joseph Stalin. The Soviet ruler reputedly chose a French-sounding name to insinuate a Western origin. Yet all of these origin stories are disputed. In a world of deception, even etymology is fraught with mistruths.

What isn’t disputed is Russia’s expertise in the field. In the Soviet era, intelligence services merged forgeries, fake news, and front groups into a playbook for political warfare. After the USSR collapsed, old strategies were embedded in new tools. Today’s tricks encompass troll farms spreading support for Kremlin views, bot armies manipulating social media algorithms, and proxy news sites amplifying falsehoods.

Ukraine is all too familiar with the tactics. The country has become a testbed for Russia’s information warfare, which has laid firm foundations for a nascent startup sector.

“It’s an enduring act — Ukraine has been waging an informational struggle against the Russian aggressor for more than 10 years now,” Denis Gursky, a former data advisor to Ukraine’s Prime Minister and the co-founder of tech NGO SocialBoost, told TNW.

“Over this time, Ukraine formed the mechanism of joint work of various sectors, which all together help to repel enemy attacks and protect the information space.”

At SocialBoost, Gursky develops civic tech and open government data. Credit: Denis Gursky

Gursky is a driving force behind Ukraine’s emerging counter-disinformation industry. In January, he co-organised the1991 Hackathon: Media, which sought digital solutions to information security challenges. One of the judging criteria was commercial potential.

The responses ranged from war crime trackers and content blockers to news monitors and verification tools. To monetise their concepts, the teams pitched an array of business plans.

Mediawise, a browser extension that adds content and author checks to online news, plans to take payment for premium features, such as alerts and extended article summaries.

OffZMI, an app that protects reliable information from a controversial Ukrainian media law, is eyeing revenues from ads, subscriptions, and NGO partnerships. MindMap, which provides Q&A translations of English-language news reports, envisions a tiered membership model.

Then there is Osavul, which won the hackathon. The company has built a platform that targets an evolving concept in the field: coordinated inauthentic behaviour (CIB).

“The problem is big enough to solve.

A term popularised by Facebook, CIB involves multiple fake accounts collaborating to manipulate people for political or financial ends. To spot this behaviour, Osavul’s AI models detect indicators including account affiliations, posting time patterns, involvement of state media, and content synchronisation.

A key component of the system is a cross-platform approach. This enables Osavu to track CIB across various social networks, online media, and messenger apps. A single campaign can, therefore, be followed from Telegram through X and then into news reports.

One such campaign claimed that NATO had donated infected blood to Ukraine. At the centre of the conspiracy theory was a fake document that purportedly proved the claim.

According to Osavul, the CIB was detected before the campaign gained momentum. Ukrainian government agencies then used the findings to refute the canard.

Dmytro Bilash (left) and Dmytro Pleshakov founded Osavul in February.

Ukrainian institutions will get free access to Osavul throughout the war, but the company has also developed a SaaS product. The software targets businesses that are vulnerable to disinformation campaigns, such as pharmaceutical companies. Osavul’s founders, Dmytro Bilash and Dmitry Pleshakov, compare it to conventional cyber security products.

“In the same way organisations protect themselves from malware or phishing, they should protect themselves from disinformation,” Bilash and Pleshakov told TNW via email. “The problem is big enough to solve, and there is a need for suppliers of software products like Osavul.”

With multilingual capabilities and the infrastructure to integrate new data sources, the platform is built to scale. “Budgets for information security are growing, so we see a huge business opportunity in this niche,” Bilash and Pleshakov said.

An early investment suggests their plan has promise. In May, Osavul raised $1mn in a funding round led by SMRK, a Ukrainian VC firm. The cash will finance a move into the international market.

That market could be ripe for expansion. A 2019 study by cybersecurity firm CHEQ and the University of Baltimore estimated that fake news costs the global economy around $78bn (€72bn) each year.

Fake news can cause dramatic stock market fluctuations. Credit: CHEQ

According to the researchers, around half of that figure comes from stock market losses. They cite an eye-popping example from 2017. That December, ABC News erroneously reported that Donald Trump had directed Michael Flynn, his former national security advisor, to contact Russian officials during the 2016 presidential campaign. Following the story, the S&P 500 Index briefly dropped by 38 points — losing investors around $341bn.

ABC didn’t retract the claim until after markets closed. At that point, the losses were down to “only” $51bn (€47bn) for the day.

Beyond the stock market, the study estimated that financial misinformation in the US costs companies $17bn (€15.9bn) each year. Health misinformation, meanwhile, causes annual losses of around $9bn (€8.4bn). The researchers said all their estimates were conservative.

A divisive business

Despite the risks to corporations, the anti-disinformation sector still depends on government backing. That foundation creates both support and frailty.

“The state can have a long-term strategy in the fight against hybrid threats because commercial and public organisations do not have the institutional stability that state bodies have,” Gurksy, the hackathon organiser, told TNW. “But the fight against disinformation is possible only in cooperation with other private and third sectors, which, in fact, have the most experience and tools in this direction.”

Government links are also a prevailing concern about anti-disinformation. Outside of Ukraine, politicians have been accused of exploiting the issue to suppress dissent and control narratives.

In the UK, campaigners found that the government’s anti-fake news units have surveilled citizens, public figures, and media outlets for merely criticising state policies. In addition, the units reportedly facilitated censorship of legal content on social media.

Caroline Lucas, the Green Party’s first MP, was included in a disinformation report for criticising the government’s response to the pandemic. Credit: Patrick Duce

Critics have also been unsettled by tech firms acting as arbiters of truth. But there are now paradoxical concerns about Silicon Valley retreating from these roles.

X, Meta, and YouTube have all been recently accused of reducing efforts to tackle disinformation. In tough economic times, these investments appear to have slipped down the list of priorities. That raises another barrier for Ukraine’s nascent startups: access to capital.

Nonetheless, there are grounds for optimism. Ukraine has a deep pool of tech talent, demonstrably resilient startups, unique experience in fighting propaganda, and strong support from international allies. Sector insiders believe this combination is a powerful launchpad for startups.

Nina Kulchevych, a disinformation researcher and founder of the Ukraine PR Army, expects her country to reap the rewards. She envisions the cottage industry evolving into a global powerhouse.

“Ukraine can be an IT hub for Europe in the creation of technologies for debunking propaganda and spreading disinformation,” she said.

In an economy devastated by war, the commercial potential of counter-disinformation is a powerful attraction. But it’s a peripheral motive for many Ukrainians in the sector. Olha Lykova, the data collection lead at Dattalion, has a separate focus: exposing the truth about Russia’s war.

“Of course, we hope that Ukraine will win,” she said. “But in any case, it will be harder to rewrite history — because we have the proof.”