Federal prosecutors have seized $15 billion from the alleged kingpin of an operation that used imprisoned laborers to trick unsuspecting people into making investments in phony funds, often after spending months faking romantic relationships with the victims.

Such “pig butchering” scams have operated for years. They typically work when members of the operation initiate conversations with people on social media and then spend months messaging them. Often, the scammers pose as attractive individuals who feign romantic interest for the victim.

Forced labor, phone farms, and human suffering

Eventually, conversations turn to phony investment funds with the end goal of convincing the victim to transfer large amounts of bitcoin. In many cases, the scammers are trafficked and held against their will in compounds surrounded by fences and barbed wire.

On Tuesday, federal prosecutors unsealed an indictment against Chen Zhi, the founder and chairman of a multinational business conglomerate based in Cambodia. It alleged that Zhi led such a forced-labor scam operation, which, with the help of unnamed co-conspirators, netted billions of dollars from victims.

“The defendant CHEN ZHI and his co-conspirators designed the compounds to maximize profits and personally ensured that they had the necessary infrastructure to reach as many victims as possible,” prosecutors wrote in the court document, filed in US District Court for the Eastern District of New York. The indictment continued:

For example, in or about 2018, Co-Conspirator-1 was involved in procuring millions of mobile telephone numbers and account passwords from an illicit online marketplace. In or about 2019, Co-Conspirator-3 helped oversee construction of the Golden Fortune compound. CHEN himself maintained documents describing and depicting “phone farms,” automated call centers used to facilitate cryptocurrency investment fraud and other cybercrimes, including the below image:

Credit: Justice Department

Prosecutors said Zhi is the founder and chairman of Prince Group, a Cambodian corporate conglomerate that ostensibly operated dozens of legitimate business entities in more than 30 countries. In secret, however, Zhi and top executives built Prince Group into one of Asia’s largest transnational criminal organizations. Zhi’s whereabouts are unknown.

A federal judge sentenced a 53-year-old Kansas man to more than 24 years in prison after the former bank CEO abused his trusted position to embezzle $47 million after falling for a cryptocurrency scam that he believed would make him wildly rich.

In a press release, the US Attorney’s Office said that Shan Hanes was driven by “greed” when directing bank employees to transfer millions in funds to a sketchy crypto wallet managed by still-unknown third parties behind the so-called “pig butchering” scheme.

Hanes was first targeted by scammers in late 2022, apparently when he got a message from an unidentified co-conspirator on WhatsApp, prosecutors said. After blowing through his own funds seeking promised profits, Hanes stole tens of thousands from a local church, then a local investor club, and finally his daughter’s college fund, NBC News reported. Then when all those wells dried up, he started stealing bank funds—all in the false hopes that sending more and more money to the scammers would somehow “unlock the supposed returns” on his crypto investments.

In total, Hanes made 11 wire transfers using bank funds between May 2023 and July 2023. But instead of getting rich quick, Hanes never realized any profits at all, the US Attorney’s Office said.

He pleaded guilty to one count of embezzlement by a bank officer after he singlehandedly caused the collapse of Heartland Tri-State Bank (HTSB) in Elkhart, Kansas, the press release said.

Because the bank was insured by the Federal Deposit Insurance Corporation (FDIC), the FDIC “absorbed the $47.1 million loss” after “Hanes’ fraudulent actions caused HTSB to fail and the bank investors to lose $9 million,” the US Attorney’s Office said. On top of those losses, Hanes’ fraudulent actions caused “catastrophic losses to bank customers who relied on the bank for the safekeeping of their savings,” the press release confirmed.

According to NBC News, Hanes missed at least one opportunity to realize that he was being scammed. After he asked for a $12 million loan from a neighbor, Brian Mitchell, his neighbor detected the scam and refused to lend the money.

“I said, ‘You’re in a scam, walk away,'” Mitchell told NBC News.

But Hanes didn’t walk away. Going the other direction, he directed bank employees to wire millions more to scammers after he got the warning from Mitchell. It wasn’t until Mitchell heard from a bank employee that Hanes had wired money out of the bank that Mitchell insisted on speaking to the bank’s board.

Days later, Hanes was fired, NBC News reported. But even then, Hanes never believed he was being scammed, reportedly telling Mitchell that he was still scheming to find a way to recover his make-believe profits right up to the moment he was arrested.

“He said … ‘If I just had another two months, I could get the money back,'” Mitchell told NBC News.

Law enforcement and government officials have warned that pig-butchering scams are growing increasingly common, urging people to “think twice” to avoid being victimized. Last year, the US Department of the Treasury’s Financial Crimes Enforcement Network issued an alert, which explained in detail how the scams commonly work and laid out red flags to watch out for.

Victims may never fully recover losses, DOJ says

A Kansas FBI agent, Stephen Cyrus, said in the press release that as CEO, Hanes violated “the trust and confidence of the community of Elkhart” by embezzling the funds.

Mitchell described Hanes’ deceptions and manipulations as “pure evil,” while Cyrus said that it was Hanes’ “job” and “the bank’s job” to “protect its customers and identify fraudulent scams—not to participate in them.”

In a court filing at sentencing, Hanes’ lawyer, John Stang, chalked up his client’s misdeeds to “bad choices,” reminding the court that Hanes had been deceived, too, by “an extremely well-run cryptocurrency scam.”

“He was the pig that was butchered,” Stang wrote. “Mr. Hanes’s vulnerability to the Pig Butcher scheme caused him to make some very bad decisions, for which he is truly sorry for causing damage to the bank and loss to the Stockholders.”

Hanes faced a maximum penalty of 30 years. While Judge John Broomes ordered him to serve less time than that, his sentence of more than 24 years is 29 months longer than prosecutors had requested, NBC News reported.

Right now, it’s unclear how or when victims will be repaid for losses. Broomes ordered “that restitution be finalized at a separate hearing within the next 90 days,” the US Attorney’s Office said.

In the community, people are still struggling to recover, Mitchell told NBC News, noting that some people lost up to 80 percent of their retirement savings. For at least one woman, retirement is impossible now, Mitchell said, and for another local woman, it has become difficult to pay for her 93-year-old mother’s nursing home.

US Attorney Kate E. Brubacher said that it’s hard to say when or if victims will be made whole again.

“Hanes is a liar and a master manipulator” who squandered away “tens of millions of dollars in cryptocurrency” while orchestrating “schemes to cover his tracks concerning the losses at the bank,” Brubacher said. “Many victims will never fully recoup losses to their life savings and retirement funds, but at least we at the Department of Justice can see that Hanes is held criminally responsible for his actions.”

Stablecoins, cryptocurrencies pegged to a stable value like the US dollar, were created with the promise of bringing the frictionless, border-crossing fluidity of bitcoin to a form of digital money with far less volatility. That combination has proved to be wildly popular, rocketing the total value of stablecoin transactions since 2022 past even that of Bitcoin itself.

It turns out, however, that as stablecoins have become popular among legitimate users over the past two years, they were even more popular among a different kind of user: those exploiting them for billions of dollars of international sanctions evasion and scams.

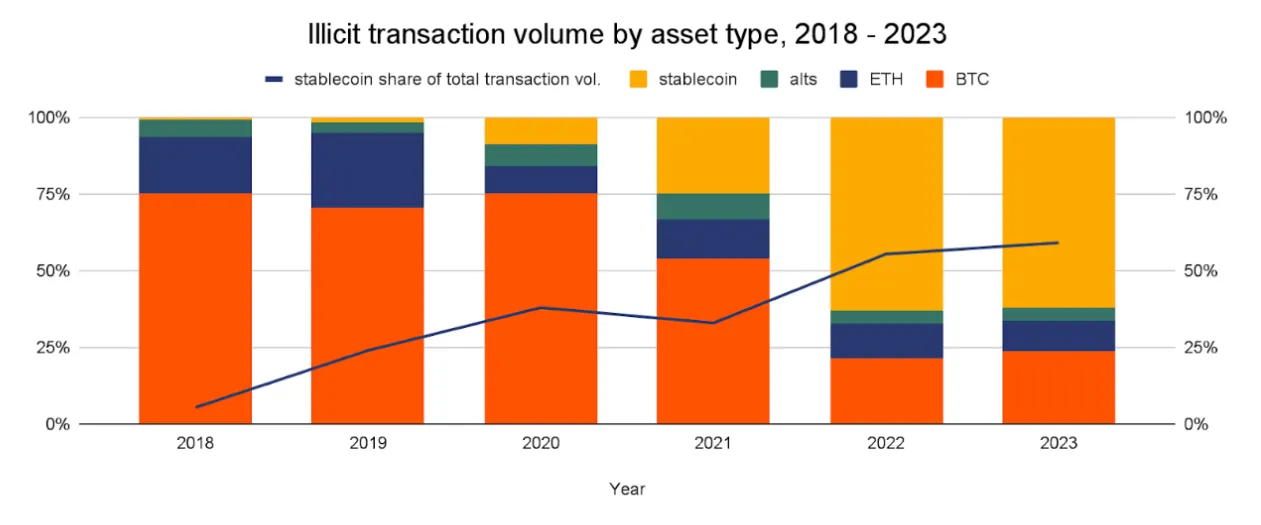

As part of its annual crime report, cryptocurrency-tracing firm Chainalysis today released new numbers on the disproportionate use of stablecoins for both of those massive categories of illicit crypto transactions over the last year. By analyzing blockchains, Chainalysis determined that stablecoins were used in fully 70 percent of crypto scam transactions in 2023, 83 percent of crypto payments to sanctioned countries like Iran and Russia, and 84 percent of crypto payments to specifically sanctioned individuals and companies. Those numbers far outstrip stablecoins’ growing overall use—including for legitimate purposes—which accounted for 59 percent of all cryptocurrency transaction volume in 2023.

In total, Chainalysis measured $40 billion in illicit stablecoin transactions in 2022 and 2023 combined. The largest single category of that stablecoin-enabled crime was sanctions evasion. In fact, across all cryptocurrencies, sanctions evasion accounted for more than half of the $24.2 billion in criminal transactions Chainalysis observed in 2023, with stablecoins representing the vast majority of those transactions.

The attraction of stablecoins for both sanctioned people and countries, argues Andrew Fierman, Chainalysis’ head of sanctions strategy, is that it allows targets of sanctions to circumvent any attempt to deny them a stable currency like the US dollar. “Whether it’s an individual located in Iran or a bad guy trying to launder money—either way, there’s a benefit to the stability of the US dollar that people are looking to obtain,” Fierman says. “If you’re in a jurisdiction where you don’t have access to the US dollar due to sanctions, stablecoins become an interesting play.”

As examples, Fierman points to Nobitex, the largest cryptocurrency exchange operating in the sanctioned country of Iran, as well as Garantex, a notorious exchange based in Russia that has been specifically sanctioned for its widespread criminal use. Stablecoin usage on Nobitex outstrips bitcoin by a 9:1 ratio, and on Garantex by a 5:1 ratio, Chainalysis found. That’s a stark difference from the roughly 1:1 ratio between stablecoins and bitcoins on a few nonsanctioned mainstream exchanges that Chainalysis checked for comparison.

Enlarge/ Chainalysis’ chart showing the growth in stablecoins as a fraction of the value of total illicit crypto transactions over time.

{kind=link}